How to conduct a double materiality assessment: A practical step-by-step guide (2026)

Learn how to conduct a Double Materiality Assessment with this practical step-by-step guide covering impact and financial materiality, IROs, stakeholder engagement, scoring, materiality matrices, and ESG reporting.

.svg)

Table of Contents

Introduction

Ask five sustainability teams how they ran their double materiality assessment (DMA) and you'll usually get five different answers, none of them especially confident. That's not a knock on the people doing the work. Double materiality is hard to run well, and most organisations are only a cycle or two into doing it at all.

Double materiality means looking at a sustainability topic from two directions at once: how the organisation affects people and the planet, and how sustainability issues affect the organisation's own finances. A topic only needs to clear one of those two bars to count as material, not both.

Organisations are no longer running these assessments purely because a regulation told them to. Investors are asking pointed questions about methodology. Customers are sending materiality-based supplier questionnaires. Boards want a defensible answer to "why does this topic matter more than that one?" This guide walks through what a DMA actually involves in practice: the governance decisions, the scoring logic, the stakeholder work, and the mistakes that undermine an otherwise solid process, drawing on how experienced sustainability teams structure the exercise rather than how a regulation describes it on paper.

What Is Double Materiality?

Every reporting framework needs some test for deciding which topics make the cut. The simplest version of that test: a topic is material if getting it wrong, leaving it out, or describing it inaccurately would change what a reader of the report decides to do.

Double materiality is a more demanding version of that test, because it asks two separate questions rather than one.

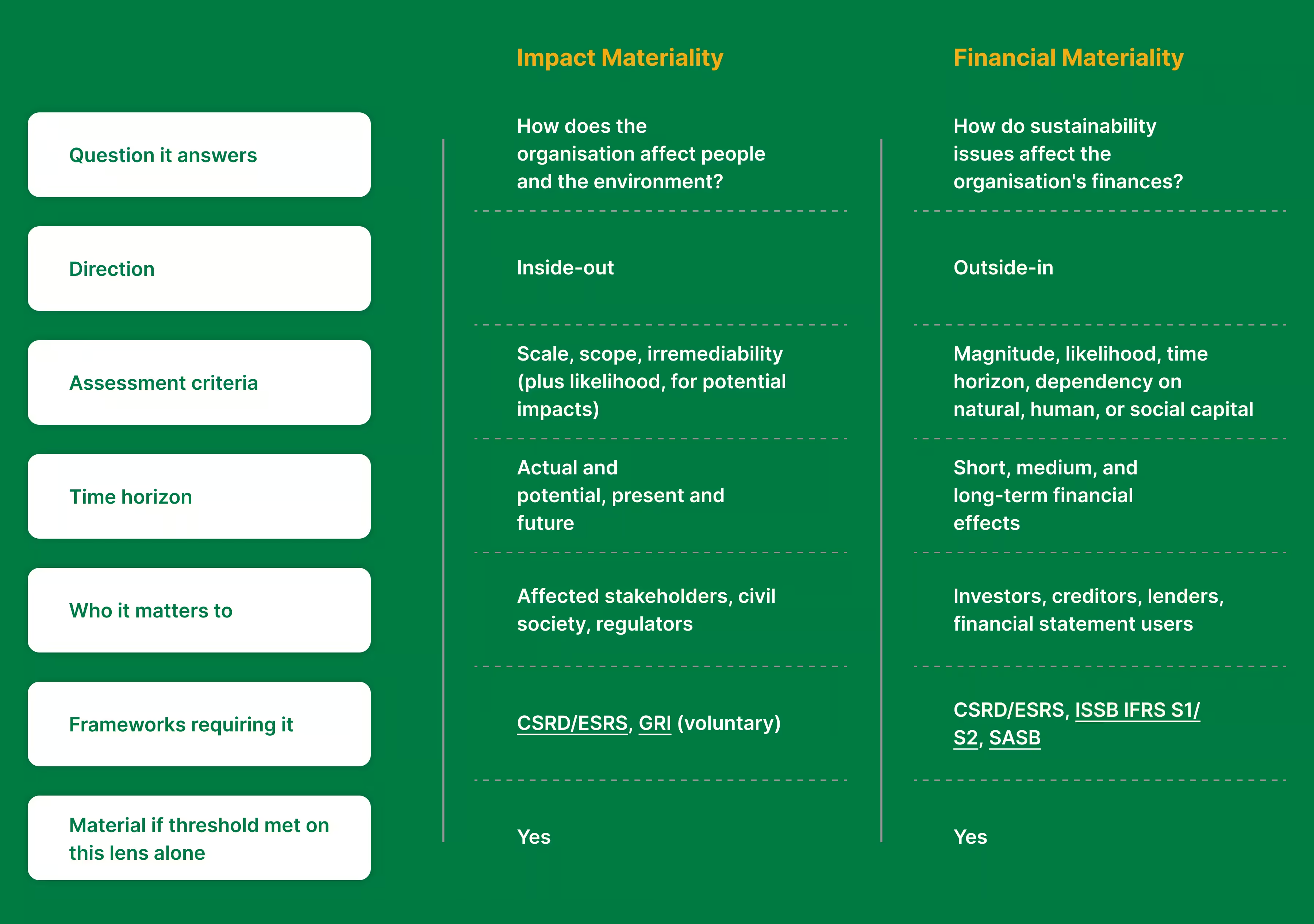

Impact materiality asks: what effect does this organisation have on people and the planet? This is an inside-out lens. It covers the company's own operations as well as its value chain, and it includes harm that's already happened as well as harm that could happen, alongside any positive effects.

Financial materiality asks: what effect could sustainability issues have on the organisation itself, its revenue, costs, balance sheet, or ability to raise capital? This is an outside-in lens, the kind of question an investor or lender would ask.

A lot of teams trip up at this point: these two questions are not an "and." A topic doesn't need to pass both tests to count as material; it only needs to pass one. A factory drawing down a water table that local farmers depend on is material even if it costs the company nothing right now. A looming supplier disruption is material even if no one outside the company will ever notice it. Treating this as an "and" test instead of an "or" test is the single most common scoping mistake, and it means the organisation will end up disclosing far less than it should. This OR logic carries through every later step of the process, including how scoring works (Step 7) and how topics land on the final materiality matrix (Step 8).

Impact Materiality vs. Financial Materiality

Why Does Double Materiality Matter?

Most organisations come to double materiality because a regulation made them. That's a fine starting point, but it undersells what a properly run assessment actually delivers and treating it purely as a compliance exercise is exactly how organisations end up with a thin, defensible-on-paper-only document.

Better ESG strategy. Run well, a DMA gives leadership something they rarely have otherwise: a ranked, evidence-backed view of which sustainability issues actually matter to the business, rather than a list of themes everyone half-agrees on. That clarity makes budget and priority decisions noticeably easier.

Better risk management. Scoring an IRO properly, a supplier's exposure to water stress, say, or physical climate risk at a specific facility, often surfaces a gap in the existing risk register long before it would otherwise come to light.

Investor confidence. It's no longer enough to list the topics a company reports on. Institutional investors and rating agencies increasingly want to see the reasoning behind why those topics were chosen, and a documented DMA is the easiest way to have that answer ready.

Stakeholder trust. Structured engagement with workers, suppliers, and affected communities, done with any real follow-through, tells those groups the organisation is listening rather than going through the motions of consultation.

Resource prioritisation. Sustainability functions rarely have the headcount or budget to chase every possible issue. A materiality assessment is what tells them where that limited attention will do the most good.

Reporting efficiency. It pays off across multiple reporting obligations at once. Once topics are properly scored and mapped, that same underlying work can support CSRD, GRI, ISSB, and BRSR disclosures without starting from scratch each time.

Better board discussions. A matrix backed by real scoring gives directors something concrete to interrogate, rather than a generic list of themes nobody can explain the reasoning behind.

Taken together, these benefits explain why double materiality has become the foundation that ESG strategy and reporting sit on, rather than a side exercise that runs alongside them.

Who Should Conduct a Double Materiality Assessment?

Companies reporting under CSRD. For organisations within scope, a DMA isn't optional. ESRS 1 makes it a legal requirement, and it's also the single document an assurance provider will dig into hardest.

Companies preparing GRI or BRSR reports. Neither GRI nor BRSR legally requires double materiality the way CSRD does, but a growing number of organisations adopt the methodology voluntarily anyway, simply because it produces a far more defensible basis for choosing material topics than an informal stakeholder survey ever will.

Companies responding to customers, investors and lenders. Plenty of organisations run a DMA because the market is asking for one, regardless of what regulation requires. EU customers are sending supplier questionnaires built around materiality concepts. Banks and institutional investors are folding materiality-based questions into due diligence. None of this respects company size or domicile: organisations in India, the UAE, and the UK are seeing these requests show up regardless of their own reporting status.

Organisations building ESG strategies with no external reporting obligation at all. This is the most interesting group. They run a DMA because the output, a ranked, evidence-based view of what matters, is simply more useful as strategic input than any generic ESG checklist could be.

How to Conduct a Double Materiality Assessment

The overall flow, end to end, looks like this:

Scope → Long List → Peer Benchmarking → IRO Identification → Stakeholder Mapping → Stakeholder Engagement → Scoring → Materiality Matrix → Reporting

What follows is each of those steps in practice, with the judgment calls and pitfalls that tend to separate a credible assessment from one that falls apart under a follow-up question.

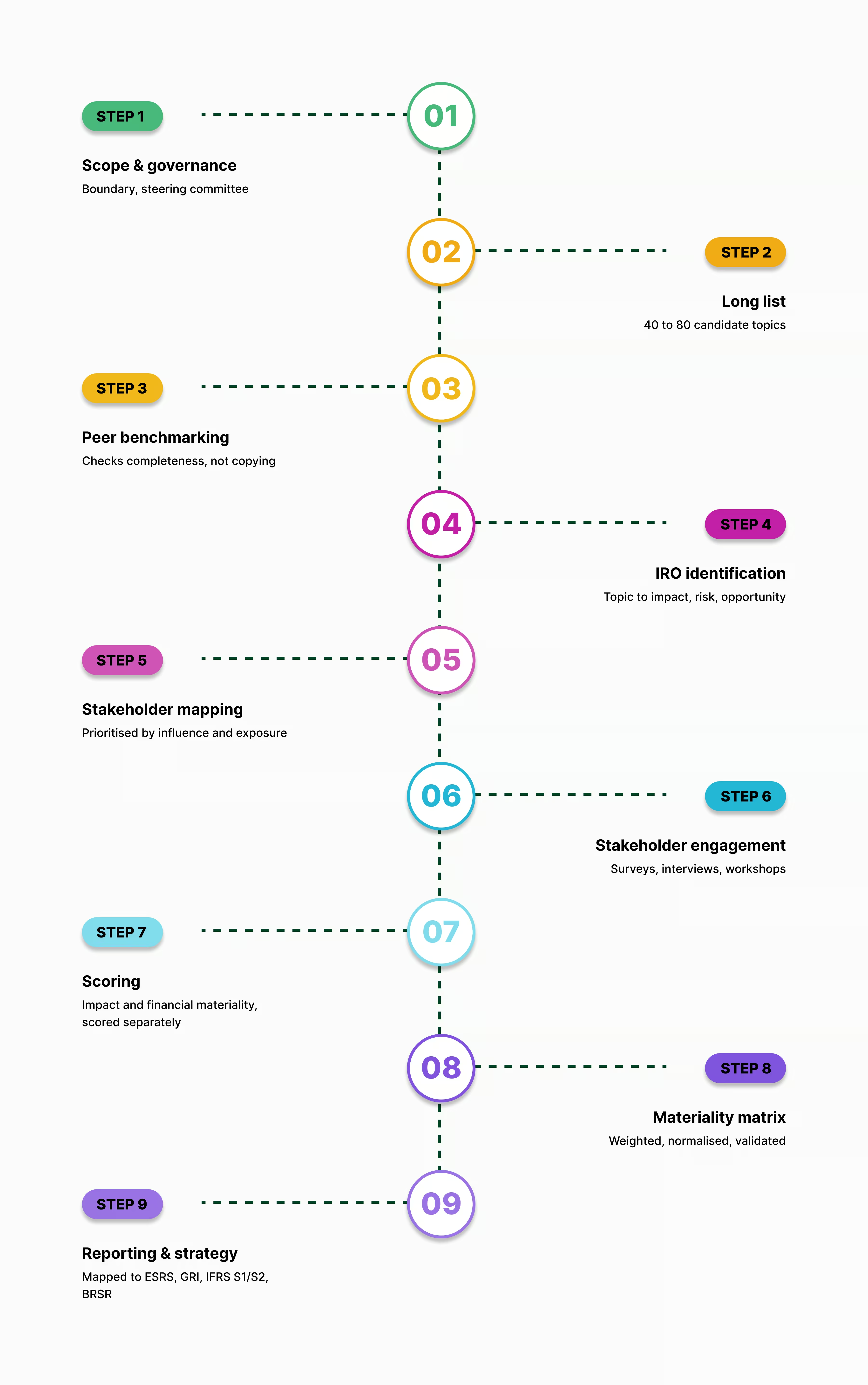

Step 1: Define the Assessment Boundary and Governance

Before a single topic gets scored, two decisions need to be settled: what the assessment covers, and who owns it.

Scope has two parts. The organisational boundary determines which entities, business units, and geographies are in play. The value chain boundary determines how far the assessment reaches upstream into suppliers and downstream into customers and end users. Get this wrong in either direction and the whole exercise suffers: scope it too narrowly and the team misses material impacts sitting a tier or two back in the supply chain; scope it too broadly and the process becomes impossible to resource.

Ownership matters just as much as scope, and it's where a lot of assessments go wrong. Leave the DMA entirely in the sustainability team's hands, with no named ownership from finance, risk, legal, or operations, and what comes out the other end tends to be a reflection of what the sustainability team already believed, not a cross-functional read on the business. Organisations that avoid this set up a small steering committee at the start, typically five to eight people drawn from sustainability, finance, risk, legal, and a senior operations or supply chain voice, with real authority to sign off on scope, agree thresholds, and settle disagreements in scoring. That committee doesn't need to meet constantly, but it needs to exist before Step 2 starts, not get assembled after scoring is already underway.

Step 2: Build the ESG Topic Universe

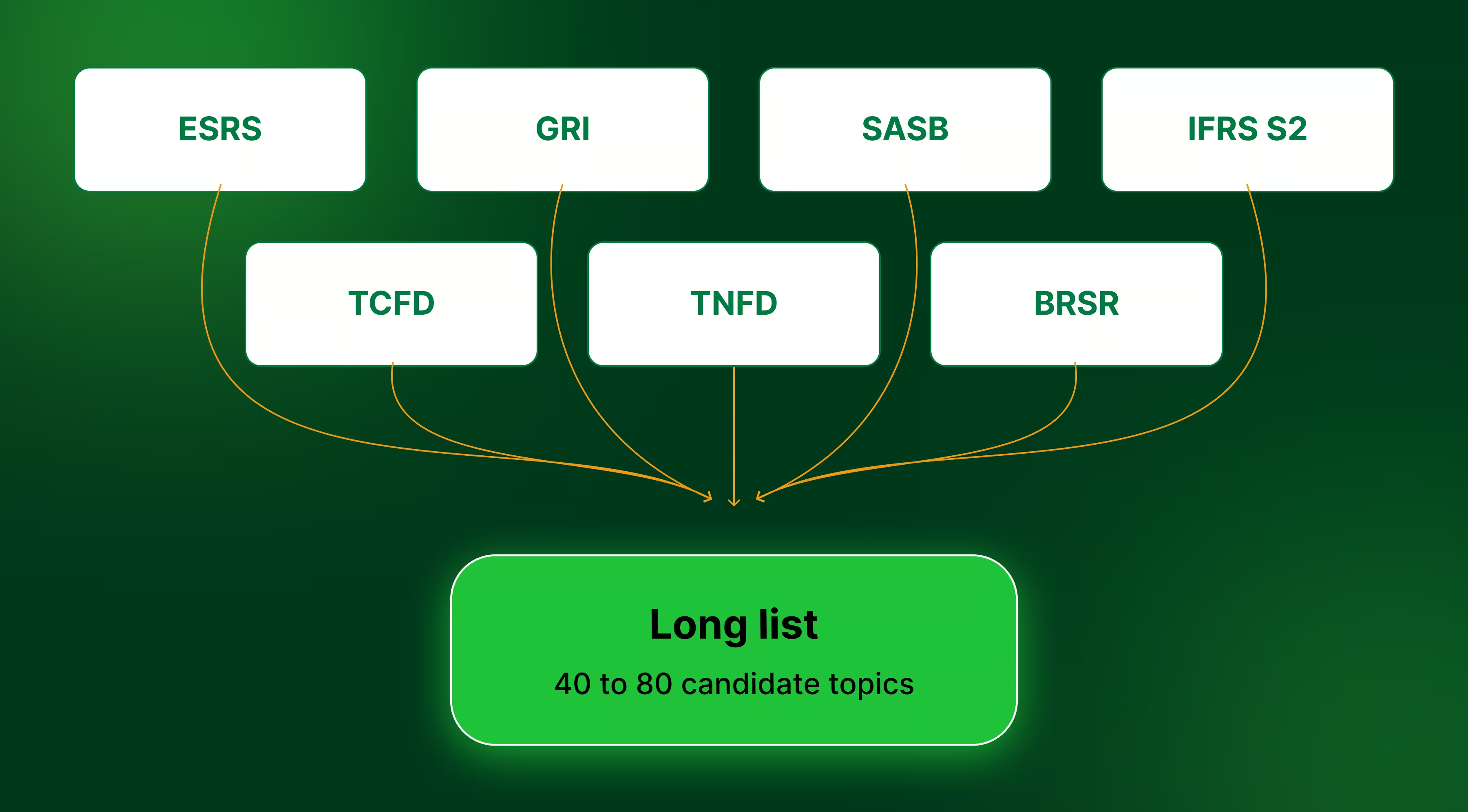

This step generates the raw material everything else will work from: a long list of candidate topics. The natural starting point is the ESRS 1 Annex AR 16 topic list, which offers the broadest existing inventory spanning environmental, social, and governance areas.

From there, most teams pull in additional frameworks to round out blind spots that any single list would otherwise leave. GRI's topic standards add a stakeholder-impact angle that ESRS alone doesn't fully capture. SASB contributes industry-specific materiality maps that surface financially relevant issues particular to a given sector. IFRS S2 contributes climate-specific financial risk thinking aligned with investor expectations, while TCFD, the framework IFRS S2 itself builds on, adds its own established categories for climate governance, strategy, risk management, and metrics that some teams still reference directly. TNFD adds nature and biodiversity topics that matter for sectors with land, water, or ecosystem dependencies, and BRSR contributes topics specific to Indian-listed companies (see KarbonWise's guide to BRSR for a fuller breakdown of what it covers). On top of the frameworks, sector regulation, prior investor engagement, internal strategic priorities, and direct customer requirements all feed into the same list.

For a mid-size organisation, this process usually lands somewhere between 40 and 80 candidate topics before any scoring happens, and that range isn't accidental. Teams that compress the list too early, cutting it down to 15 or 20 topics before a single score has been assigned, tend to produce assessments that read as pre-decided rather than analytically derived. That's exactly the pattern assurance providers and engaged stakeholders are trained to notice.

Step 3: Peer Benchmarking and Industry Review

Before any stakeholder is approached, the long list should be checked against what peers in the same sector are actually disclosing. That means pulling sustainability reports, annual reports, ESG ratings, and public disclosures from comparable companies, and looking at what topics they've treated as material, how mature their governance and disclosure practices are, and what emerging issues they've flagged that the internal list may have missed.

The point of this exercise is to check completeness, not to copy what competitors are doing. If every other company in the sector treats a particular issue as material and it never surfaced internally, that's worth investigating on its own merits, not adopting wholesale because a competitor did it first.

Doing this benchmarking before stakeholder engagement begins, rather than after, has a real payoff: the questions put to stakeholders in Steps 5 and 6 arrive already informed by what the wider industry considers relevant, which tends to produce sharper engagement than starting from a blank page.

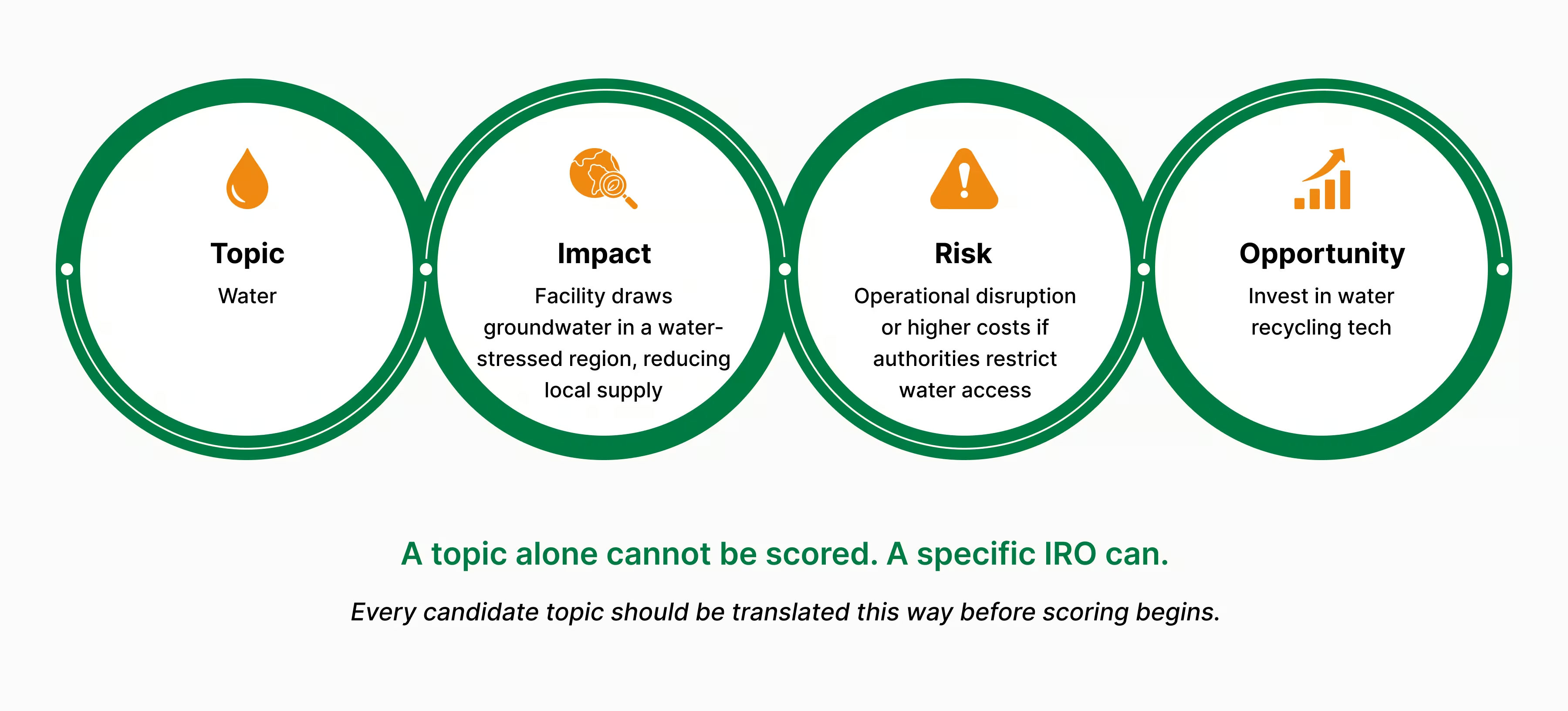

Step 4: Translate Topics into IROs

This is the most consequential step in the entire process, and the one most assessments get wrong structurally. A topic on its own, such as "water," "labour practices," or "climate change," sits too high-level to score or to trace to a specific disclosure requirement. What can be scored is a specific Impact, Risk, or Opportunity (IRO) derived from that topic.

A worked example makes the logic concrete. Take water as the starting topic. The impact is something specific: a manufacturing facility drawing groundwater in a region already classified as water-stressed, reducing what's available to surrounding communities and farms. That same dependency produces a risk: operational disruption or rising costs if local authorities tighten water restrictions, plus reputational exposure if the impact becomes public. And sitting alongside that risk is an opportunity: investing in water recycling and efficiency technology, which addresses the impact and reduces the long-term cost exposure at the same time.

Every topic on the long list should go through this same translation before scoring starts. If a topic can't be broken down into at least one specific IRO, that's usually a sign it was too generic to begin with, and it should either be sharpened into something concrete or set aside, with the reason for setting it aside written down.

Step 5: Stakeholder Mapping

Engagement can't be designed well without first mapping who actually needs to be engaged. Internally, that typically means operations, procurement, finance, legal, HR, and senior leadership, each of whom sees a different slice of the picture. Externally, the list is broader still: employees and worker representatives, suppliers across different tiers, customers, investors and lenders, regulators, and, where relevant, affected communities, NGOs, and civil society groups.

Not everyone on that list warrants the same depth of engagement, and trying to give them all equal weight is how engagement programmes become unmanageable. Prioritisation usually comes down to two questions: how much influence does this stakeholder hold over the organisation's strategy or reputation, and how directly exposed are they to the organisation's actual impacts? A tier-one supplier that scores highly on both counts, heavy influence over production and heavy exposure to labour-related impacts, belongs at the top of the list for a structured conversation. A stakeholder with low scores on both fronts can usually be reached through a lighter-touch survey instead.

Step 6: Stakeholder Engagement

With the map in hand, the actual engagement can begin, and the right method depends on who's being reached and how much depth the conversation needs.

Surveys suit broad, lower-priority groups where the goal is reach rather than depth. Interviews, structured one-on-one or small-group conversations, work better for high-priority internal experts and key external voices like major suppliers or investor representatives, since they allow for follow-up questions and pick up nuance a survey form simply can't capture. Workshops bring multiple stakeholders into the same room (or call) at once, useful for validating a shortlist of topics or working through disagreement between groups who see the same issue differently. Questionnaires sit somewhere between a survey and an interview. It's more structured than an open survey, and particularly useful when an organisation needs comparable, quantifiable answers across a large supplier base.

What comes out of this engagement should actively reshape the long list built in Step 2, not just confirm it. Topics that stakeholders keep raising unprompted deserve to move up for scoring, even if they didn't rank highly on the original framework-driven list. Topics nobody raises, despite sitting on multiple framework checklists, become candidates for de-prioritisation, though never for outright removal without a documented reason.

Step 7: Assess Impact and Financial Materiality

Scoring works best as two separate exercises rather than one blended process, partly because the two lenses use different criteria, and partly because they're often best evaluated by different people on the steering committee.

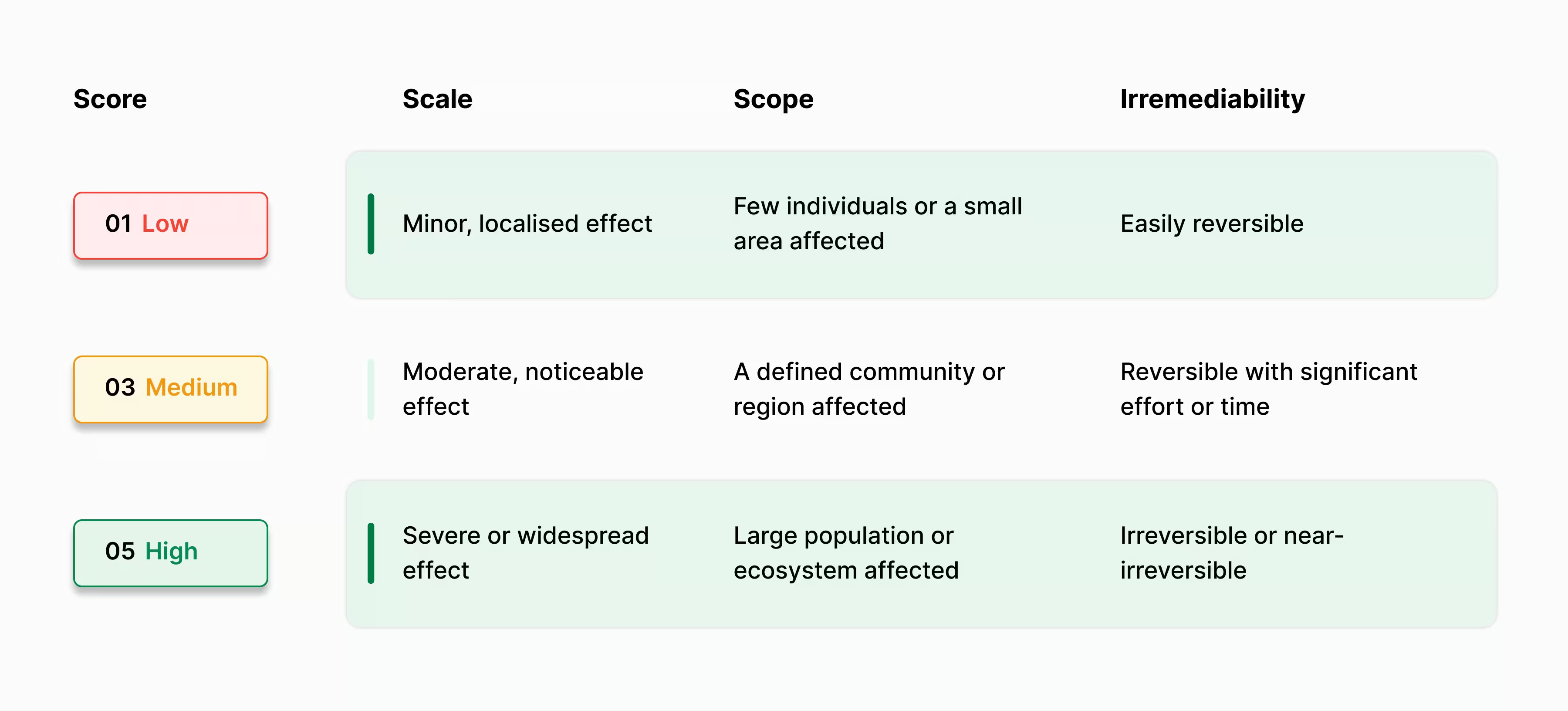

Impact materiality. The primary scoring dimension is severity, built from three sub-factors: scale (how grave or far-reaching the impact is), scope (how many people or how much of the environment is touched), and irremediability (whether the harm can be undone). For impacts that haven't happened yet, severity gets combined with likelihood. There's one rule teams routinely overlook: for potential negative human rights impacts, severity overrides likelihood entirely. A severe but improbable harm still counts as material.

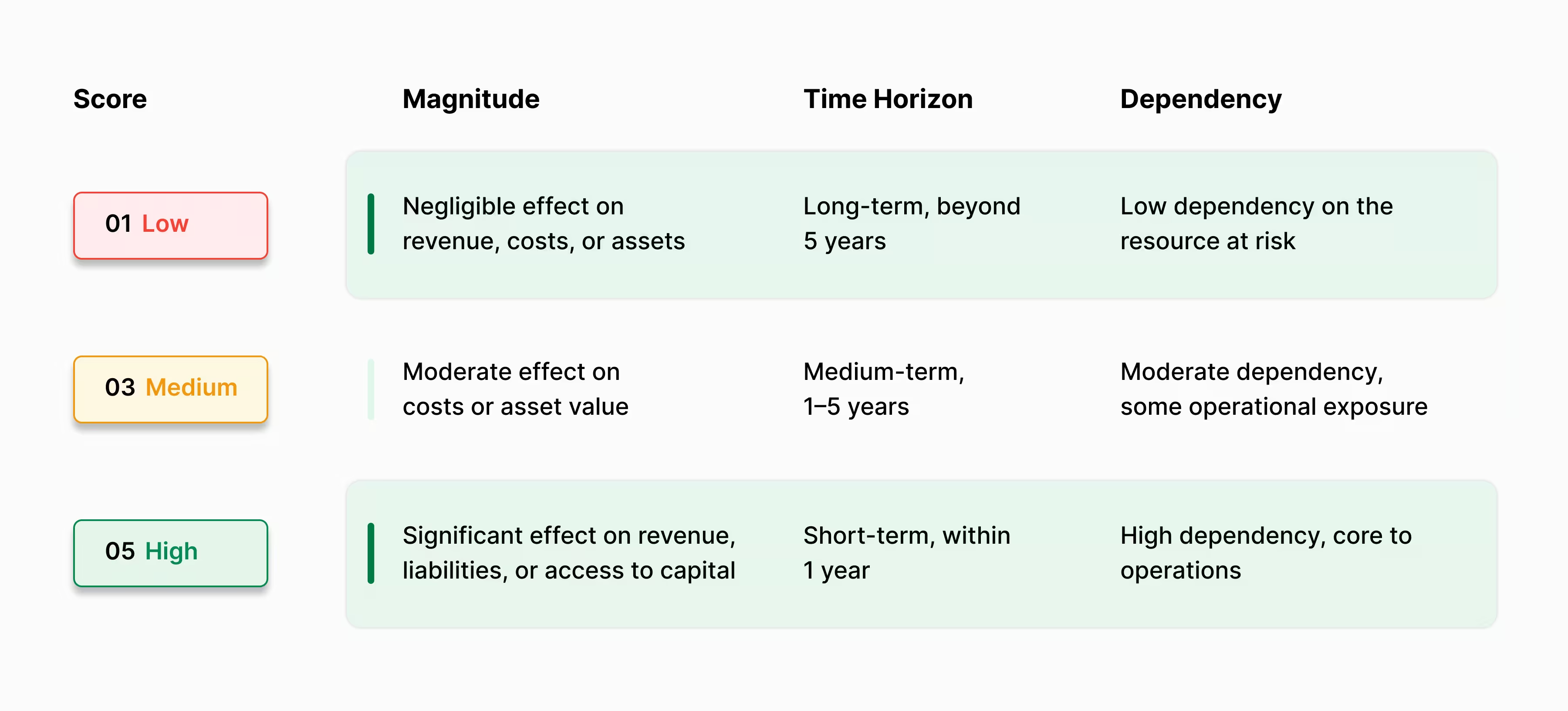

Financial materiality. Each IRO is scored on magnitude, likelihood, and time horizon, with an eye on how dependent the organisation is on natural, human, or social capital. Magnitude is where most of the judgment happens, and it is worth breaking into the specific channels a sustainability issue can actually hit: revenue, where a shift in customer demand or a lost contract changes the top line directly; costs, where rising input prices, compliance spend, or insurance premiums squeeze margins; assets, where a facility's valuation drops because of physical climate exposure or a stranded-asset risk; liabilities, where regulatory fines or legal exposure create a balance sheet impact; and reputation, which is harder to quantify but shows up eventually in customer attrition, talent retention, or cost of capital. Scoring an IRO against all five gives the steering committee a clearer picture than a single blended "financial impact" rating ever could.

Tying the financial materiality scoring back to the organisation's existing enterprise risk register at this stage, while there's still time, pays off later. Doing so heads off the most uncomfortable question an assurance provider can ask later: why a risk significant enough to disclose in the sustainability statement never showed up in the financial filing.

Going back to the water example from Step 4 shows how this actually plays out. On the impact side, the groundwater drawdown scores a 5 on scale, since it's a severe, ongoing effect on a community already short of water, a 3 on scope, since it's a defined region rather than a sprawling river basin, and a 3 on irremediability, since aquifer recovery is possible but slow. On the financial side, the same issue scores a 3 on magnitude for now, a moderate effect on costs through tighter water permits, but the time horizon sits at a 5, since local authorities are already signalling restrictions within the year, and dependency scores a 5, since this single facility supplies a meaningful share of the organisation's output. Two separate scores, two separate stories, and both point toward the same conclusion: this is a topic the assessment cannot afford to drop.

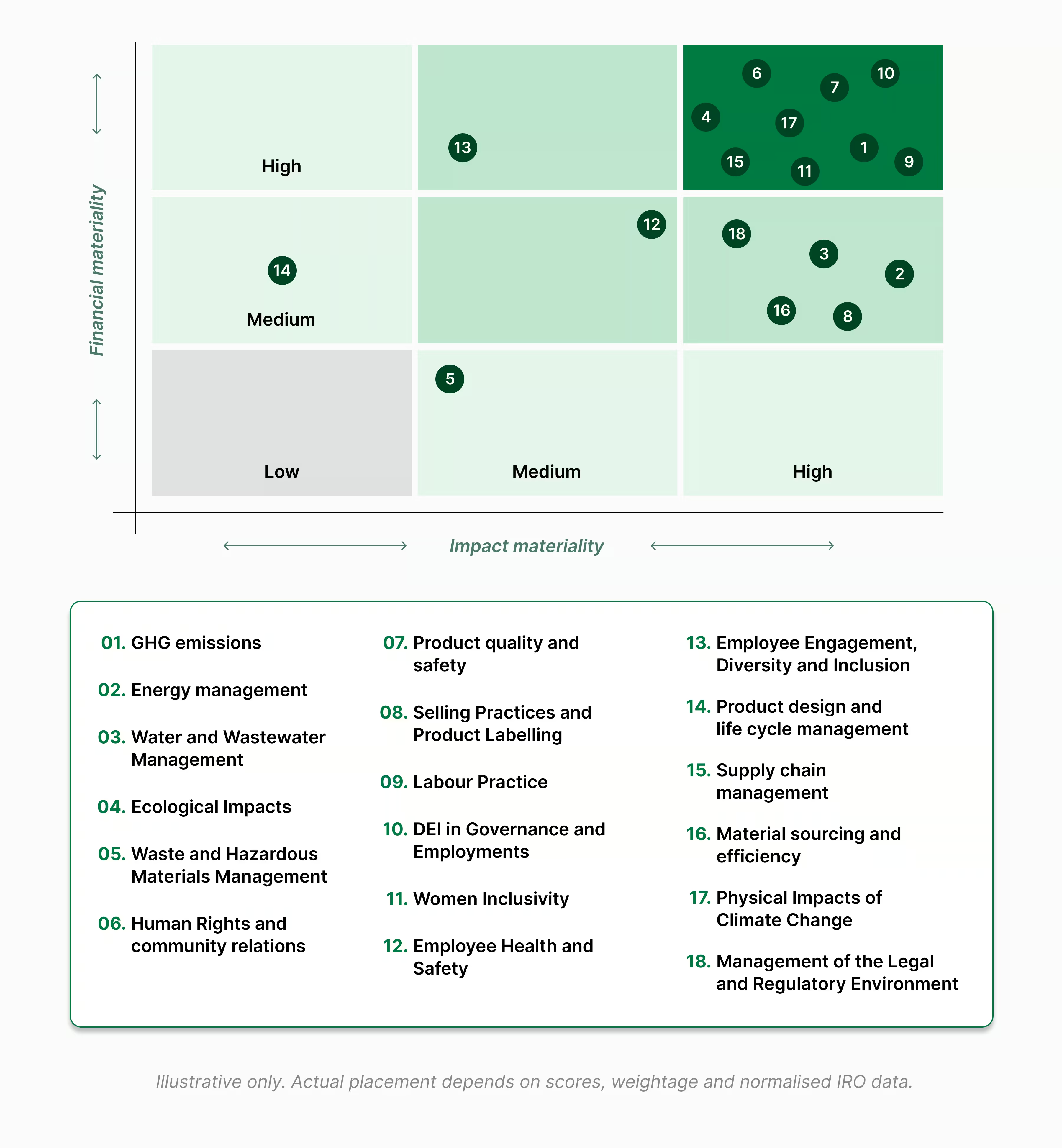

Step 8: Develop the Double Materiality Matrix

Getting from individual IRO scores to a finished matrix involves a sequence of steps, and rushing any of them is usually what produces a matrix that can't survive a follow-up question. Scoring is the easy part: it just gives raw numbers for each IRO across both lenses. What happens next is where most assessments lose rigour.

Some organisations apply weighting, adjusting for whichever criteria they consider more decisive in their specific context, irremediability for a manufacturer with heavy environmental exposure, say, or financial magnitude for one whose investors care more about the numbers than the narrative. Whether or not weighting is used, the impact and financial scores still need normalisation onto a shared scale before they can sit on the same axes, since the two are measuring fundamentally different things and a 5 on one side does not automatically mean the same as a 5 on the other. The cut-off above which a topic counts as material, the threshold, has to have been set during the methodology stage, well before any of this scoring happened, not adjusted afterward to fit however the numbers landed. Once all of that is settled, plotting produces the matrix itself, typically with impact materiality on one axis and financial materiality on the other.

The matrix isn't the end of the process. Senior leadership, and the board where appropriate, should run validation workshops to look specifically at topics sitting close to the threshold, where a small shift in judgment could push a topic in or out of the final material list. Anything that scored just below threshold deserves a second look in light of strategic context, and that review should be documented either way. Reviewers and assurance providers expect to see the reasoning behind a borderline call, not just where the dot ended up on the matrix.

The water topic from Steps 4 and 7 is a good illustration of why this matters. With an impact score built from a 5, a 3, and a 3, and a financial score pulled up by that short time horizon and high dependency, it lands well inside the material zone on both axes, nowhere near a borderline call. A validation workshop wouldn't need to spend much time on it. The topics worth that scrutiny are the ones sitting one point either side of the threshold, where the steering committee's judgment, not the raw arithmetic, ends up deciding the outcome.

Step 9: Translate the DMA into Reporting and Strategy

None of the preceding analysis is worth much if it doesn't feed directly into what the organisation does next. Each material IRO needs to be mapped to the disclosure requirements it actually supports, which in practice means matching it against whichever of the four frameworks the organisation reports under: ESRS topical standards for CSRD, GRI topic standards for stakeholder-facing reporting, IFRS S1 and S2 for investor-focused disclosure, and BRSR for Indian-listed companies. Because each IRO is already tagged as impact-material, financial-material, or both, the same underlying analysis can serve multiple frameworks without redoing the work from scratch for each one.

Beyond disclosure, this same material topic list gives the organisation's ESG strategy a real foundation: a tested starting point for where to invest, rather than a strategy built around themes nobody formally examined. The results should ripple outward. They should shape targets prioritised around the topics that actually scored highest, update the risk register so financially material sustainability risks sit alongside the organisation's existing operational and financial risks, and inform what the board sees, giving directors a structured view of which sustainability issues carry real strategic weight.

Common Mistakes

Most double materiality assessments don't fail because the methodology was wrong on paper. They fail because a handful of shortcuts creep in once the team is under deadline pressure.

Weak stakeholder engagement is the biggest one. ESRS 2 IRO-1 explicitly requires consultation with affected stakeholders, yet what most teams produce is a survey nobody follows up on. Five or six structured interviews with the right internal experts, paired with targeted outreach to key suppliers and worker representatives, beat a 200-person survey with no documented follow-through every time.

Poor documentation is close behind. A scoring scale defined after the scoring is already done isn't a methodology, it's an explanation written backwards. Every included and excluded topic needs a written reason, and every threshold needs to exist before a single IRO is scored, not after the matrix already looks the way someone wanted it to.

A third habit, analysing at the topic level instead of the IRO level, looks fine right up until an auditor asks a follow-up question. "Climate change" sits too high-level to trace to anything. A specific emission source or a named facility's flood risk can be traced; a generic theme can't.

The last two are shorter but just as common: no value chain consideration, since material impacts are frequently concentrated upstream or downstream rather than inside an organisation's own four walls, and poor scoring methodology, where inconsistent criteria and shifting thresholds produce a matrix that looks polished but can't survive a single direct question about how a topic landed where it did.

What Changed Under the Omnibus Package?

In early 2026, the EU's Omnibus I Directive, formally Directive (EU) 2026/470, adopted by the Council on 24 February 2026 and in force from 18 March 2026, narrowed the pool of companies subject to mandatory CSRD reporting, raising the threshold to organisations with more than 1,000 employees and net turnover above €450 million, with a separate €450 million/€200 million test for third-country parent companies. A large share of previously in-scope companies are no longer required to report under CSRD at all.

Reporting itself was also simplified. The European Commission's draft revised ESRS, published 6 May 2026, cuts total datapoints from roughly 1,073 to around 320, a reduction of more than 70%. Mandatory datapoints alone fall by just over 60%, and every voluntary datapoint has been eliminated, meaning whatever remains is mandatory by default. The Commission is required to adopt the revised standards within six months of Omnibus I entering into force, with the new ESRS applying from financial year 2027, though Parliament and Council scrutiny could push final entry into force slightly later.

What did not change is double materiality itself. It remains a legal requirement for every company still within CSRD scope, and if anything matters more now than before the Omnibus, not less. With far fewer mandatory datapoints to report, a weak materiality assessment used to be partially obscured by sheer reporting volume. That cover is gone. The reasoning behind what gets disclosed, and why, is now far more exposed during a limited assurance engagement than it was under the original ESRS.

The regulatory obligation and the commercial expectation are two separate things, though. Companies that fall outside the revised CSRD thresholds aren't necessarily off the hook in practice. Banks, institutional investors, and ESG rating agencies haven't narrowed their own data requirements, and EU customers continue sending materiality-based questionnaires to suppliers regardless of company size. For organisations in India, the UAE, and the UK supplying EU markets, double materiality often remains relevant well beyond what CSRD technically requires of them.

The regulation got smaller. The judgment required to get it right did not.

Double Materiality Assessment Checklist

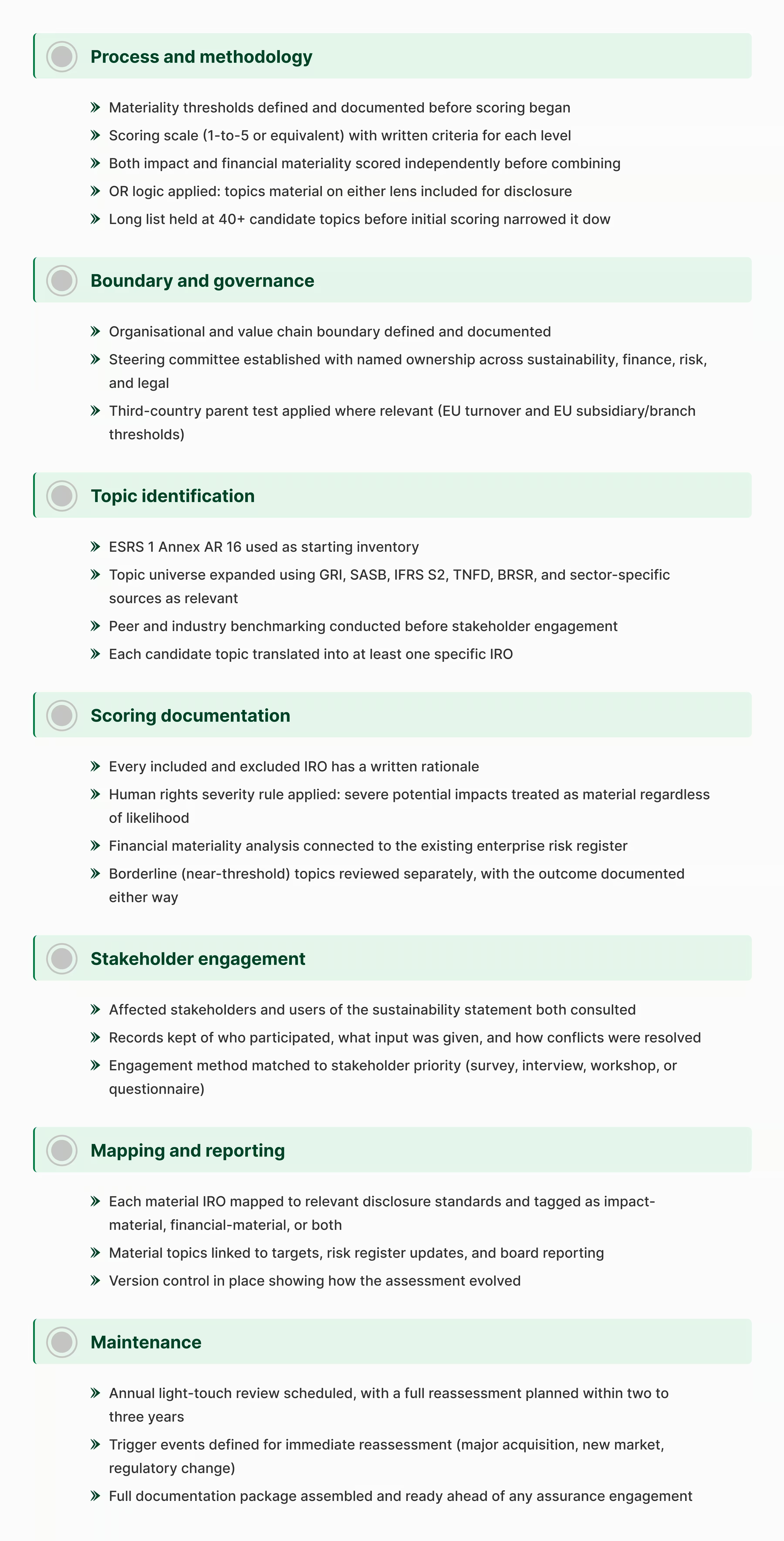

Use this before submitting a sustainability statement or entering a limited assurance engagement. Some items below trace directly to specific requirements in ESRS 1, ESRS 2, and EFRAG Implementation Guidance 1, scoring rationale, the human rights severity rule, and IRO-to-framework mapping among them. Others reflect practitioner convention rather than a documented regulatory requirement, governance structure, topic-sourcing approach, and review cadence in particular. Both are worth tracking, but only the first group is something an assurance provider can hold you to.

From Assessment to Action

A double materiality assessment that ends up filed away the moment the report ships has missed the point. Run properly, it generates several concrete things an organisation should keep using long after the disclosure deadline passes.

The most visible of these is the materiality matrix, which gives a clear, evidence-based snapshot of which topics rank highest on impact, financial relevance, or both. Just as useful, though less visible, is the underlying topic-by-topic breakdown of risks and opportunities: the specific IROs identified earlier in the process, scored against both lenses, which gives leadership something they can act on rather than just a list of themes.

From that base, organisations end up with a framework mapping that shows exactly which material topics support which disclosure requirements: ESRS, GRI, IFRS S1/S2, BRSR, so the same underlying work can serve several reporting obligations without duplicating effort. They also get a reporting roadmap, a clear sense of what needs disclosing, under which framework, and by when, plus governance documentation: the audit trail of thresholds, scoring rationale, stakeholder records, and sign-offs that an assurance provider will want to see in full.

That kind of structured output is hard to maintain across spreadsheets and scattered email threads, especially once an organisation is running this process across several business units or multiple reporting cycles. That's the gap KarbonWise is built to close. The platform guides IRO identification against ESRS 1 AR 16, keeps scoring consistent across teams, tracks stakeholder engagement with a timestamped audit record, and maps material topics directly to ESRS, GRI, and BRSR disclosure requirements. You can read more about the KarbonWise double materiality and gap assessment service or request a demo to see how it works in practice. When an assurance provider asks how a topic was scored, or who was consulted and what they said, the answer is already logged and ready to pull up, not reconstructed after the fact.

For organisations across India, the UK, and the UAE navigating CSRD exposure, voluntary GRI or BRSR reporting, or simply trying to build a more defensible ESG strategy, KarbonWise provides the structured backbone that turns a double materiality assessment from a one-off compliance exercise into something the organisation can run, repeat, and actually trust.

{{cta}}

{{accordion}}

{{sources}}

Continue Reading

Primary vs Secondary Emissions Data: Key Differences and When to Use Each

Learn the key differences between primary and secondary emissions data, when to use each, and how better data quality supports more accurate carbon accounting and Scope 3 reporting.

CBAM in 2026: The Cost Is Small Today. Here Is Exactly How It Compounds

CBAM costs may seem small today, but they increase significantly over time. Discover how the phase-in schedule, default values, and compliance obligations affect exporters through 2034.

LEED v5, Embodied Carbon, and the Whole-Lifecycle Mandate: What Project Developers and Asset Owners Need to Know

LEED v5 introduces a whole-life carbon approach to building certification, making embodied carbon assessment a key requirement for project developers, asset owners, designers, and investors.

.avif)

.svg)

.svg)