EU Taxonomy: Turning Sustainability Data into Financial Confidence

The EU Taxonomy is redefining how sustainability performance connects to financial reporting, helping organisations assess, report, and improve the environmental impact of their economic activities.

.svg)

Table of Contents

There is a point many sustainability teams recognise. Someone in the room asks whether their company’s economic activities align with the EU Taxonomy, and suddenly everyone leans forward. It is not that the regulation is new. It is that the level of transparency it demands forces organisations to examine their operations in ways that financial statements alone cannot capture. The EU Taxonomy is becoming one of the most influential sustainability frameworks in Europe because it ties environmental performance directly to financial understanding. It clarifies what counts as sustainable, what does not and where companies must improve.

The Taxonomy aims to move markets towards activities that support long-term environmental resilience. It takes the guesswork out of sustainability claims by introducing well-defined criteria across sectors. It also encourages companies to assess their operations against measurable standards. For organisations across Europe, the Taxonomy is more than another regulation. It is a signal that sustainability information now holds real financial relevance.

Why the EU Taxonomy Matters Today

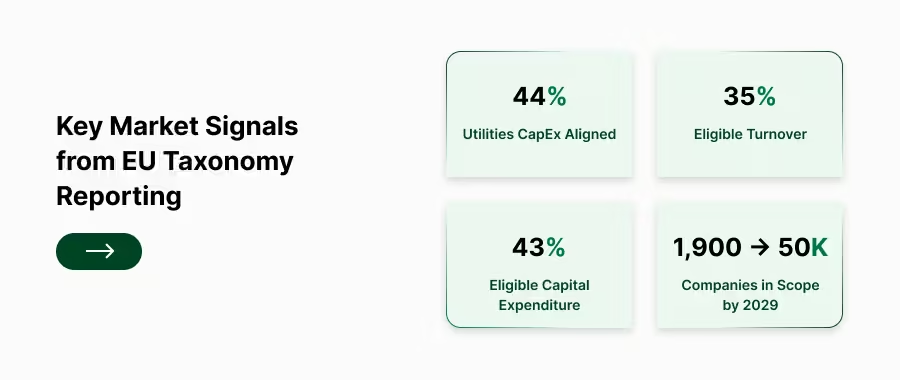

One of the clearest indicators of the Taxonomy’s impact is the rapid growth in alignment and investment reporting. European Commission analysis shows that reported EU Taxonomy alignment of capital expenditure remains limited overall, with utilities showing the highest alignment rates, reaching around 44 percent. This is a tangible sign that organisations are shifting resources into activities that meet environmental criteria.

At the same time, reporting expectations continue to expand. As organisations deepen their understanding of eligible and aligned activities, market investigators note that eligible turnover averages around 35 percent and eligible capital expenditure sits near 43 percent across reporting companies, both of which reflect increased familiarity with the framework. These numbers help organisations benchmark progress and identify areas where improvements are most needed.

The Taxonomy’s reach is also growing rapidly. Today, around 1,900 companies are in scope for mandatory EU Taxonomy disclosure, but this number is expected to rise to nearly 50,000 companies by 2029, reflecting the expansion under the Corporate Sustainability Reporting Directive. These figures reflect both regulatory ambition and market demand for consistent sustainability disclosures.

This shift highlights why the Taxonomy is central to European sustainability policy. It provides investors, regulators and customers with a comparable, reliable framework that supports informed decision-making.

The Core Idea Behind the EU Taxonomy

The EU Taxonomy is a classification system that defines which economic activities can be considered environmentally sustainable. It is built around six objectives: climate change mitigation, climate change adaptation, water protection, circular economy, pollution prevention and biodiversity restoration. For an activity to be aligned, it must make a substantial contribution to at least one objective, do no significant harm to the others and meet minimum social safeguards.

This model pushes organisations to move from broad environmental commitments to detailed assessments of their operations. It helps companies identify which activities support long-term sustainability and which require redesign or improvement. It also strengthens the credibility of sustainability reporting by replacing unclear claims with measurable criteria.

Industry reviews point out that companies must now disclose both the share of turnover associated with eligible activities and the share that is fully aligned with the Taxonomy’s technical criteria. This reflects the increasing emphasis on robust, transparent reporting. Clearer expectations make it easier for organisations to understand where they stand and how to improve.

What the EU Taxonomy Requires from Organisations

The Taxonomy requires companies to assess their activities against technical screening criteria and determine whether they are eligible or aligned. Companies must then calculate and report the proportion of turnover, capital expenditure and operational expenditure associated with these activities. They must also provide narrative explanations to help investors understand the basis of their calculations.

For many organisations, this means building new data processes, strengthening supplier engagement and improving documentation. It also requires collaboration across finance, operations, sustainability and legal teams.

The EU’s Platform on Sustainable Finance helps shape and refine the criteria, offering guidance that strengthens the application of the Taxonomy across sectors. This guidance helps organisations prepare for future updates and understand how environmental performance connects to wider economic transitions. With clearer pathways, organisations can focus their efforts where they will have the greatest impact.

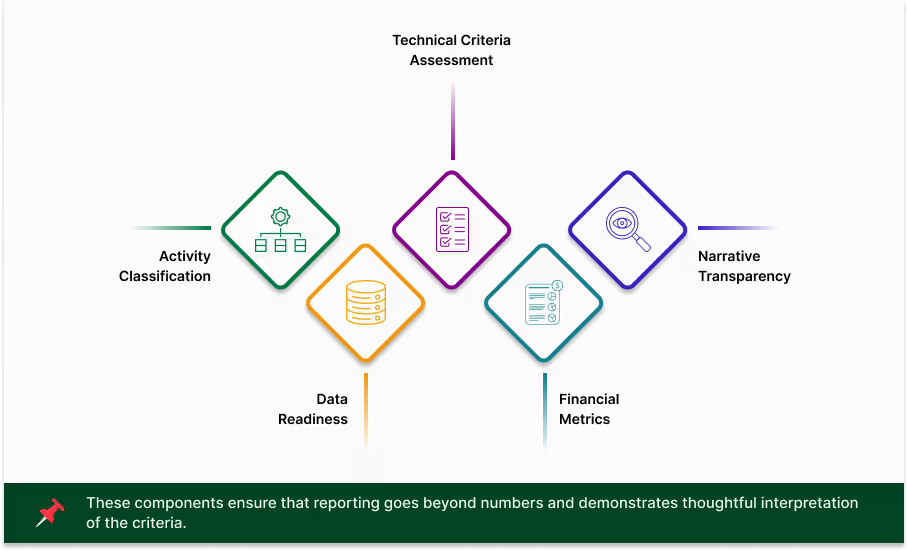

Core Components of Strong EU Taxonomy Reporting

Three Foundations for Building Taxonomy-Ready Processes

{{flipcards}}

Case Studies: EU Taxonomy in Real Organisations

Renewable Energy: Ørsted

Danish renewable energy company Ørsted has reported significant EU Taxonomy alignment within its renewable energy portfolio. As a company focused almost entirely on offshore wind and green energy generation, a large proportion of its capital expenditure qualifies under climate mitigation criteria. Clear Taxonomy alignment has strengthened investor confidence and reinforced its positioning within sustainable finance markets.

Manufacturing: Schneider Electric

Schneider Electric has integrated EU Taxonomy principles into its sustainability reporting and capital allocation processes. While not all manufacturing activities automatically qualify as aligned, the company has mapped eligible activities and adjusted operational processes to meet technical screening criteria. This has helped improve transparency in reporting and demonstrate progress towards climate and circular economy objectives.

Construction and Infrastructure: Skanska

European construction firm Skanska has applied EU Taxonomy criteria to selected real estate and infrastructure projects. By focusing on energy-efficient buildings and low-carbon construction practices, certain developments meet the substantial contribution thresholds under climate mitigation objectives. Demonstrating Taxonomy alignment has supported access to green financing and strengthened investor communication.

The Taxonomy and the Future of Sustainable Reporting

The EU Taxonomy is more than a classification system. It is becoming a cornerstone of sustainable finance, influencing how companies assess performance and how investors allocate capital. The growing number of organisations in scope reflects rising expectations around transparency and accountability.

As sustainability transitions accelerate across Europe, the Taxonomy offers a consistent way to interpret environmental performance. It helps companies turn complex operational information into a decision-ready format that supports long-term value creation.

Organisations that adopt Taxonomy processes early often find it easier to adapt to broader frameworks such as CSRD and ESRS. Many of the skills developed for Taxonomy reporting, such as data validation, scenario analysis and cross-functional coordination, are directly transferable.

Where KarbonWise Helps

KarbonWise supports organisations in navigating the EU Taxonomy by centralising operational, activity and sustainability information into a single environment. It helps teams assess eligibility, organise data consistently and link disclosures with broader reporting frameworks.

KarbonWise also assists with activity-level tracking and supplier engagement, enabling companies to understand their performance more clearly. With structured dashboards and reliable data flows, organisations can build confident, accurate EU Taxonomy reporting processes.

{{cta}}

{{accordion}}

{{sources}}

Continue Reading

SBTi FLAG Guidance v1.2: What Changed and What to Do Next

Learn what's new in SBTi FLAG Guidance v1.2, including updated deadlines, mandatory commodities, no-deforestation requirements, and practical steps for businesses.

How to conduct a double materiality assessment: A practical step-by-step guide (2026)

Learn how to conduct a Double Materiality Assessment with this practical step-by-step guide covering impact and financial materiality, IROs, stakeholder engagement, scoring, materiality matrices, and ESG reporting.

.avif)

.svg)

.svg)