What the CSRD Means for Non-EU Suppliers Exporting to Europe – An Indian Perspective

The EU’s new Corporate Sustainability Reporting Directive (CSRD) is reshaping how European companies assess their global supply chains, and Indian exporters are feeling the ripple effects. This blog explores how CSRD requirements extend beyond Europe’s borders, what they mean for Indian suppliers across key sectors, and why early alignment with ESG and Scope 3 reporting standards is becoming a competitive advantage rather than a compliance burden.

.svg)

Table of Contents

Over the past few months, in calls, meetings, and even trade events, one pattern has stood out: Indian exporters are starting to hear the term CSRD more frequently, usually in the form of last-minute queries from their European buyers. Whether it's a pharma company, an agrochemical exporter, or a mid-sized textile supplier, the story is remarkably similar. The European Union’s new sustainability disclosure regime, the Corporate Sustainability Reporting Directive, is creating ripples across value chains. But for now, most Indian businesses are still reacting to it, not preparing for it.

Because while the CSRD officially applies only to large EU companies, and non-EU firms with a significant presence in Europe, it’s their value chains that will now come under the microscope. That includes thousands of Indian suppliers who may never file a sustainability report themselves but will soon be expected to provide data that feeds into one. This growing expectation is reshaping the conversation around CSRD compliance for non-EU suppliers, pushing them to align their practices even if the regulation doesn’t apply to them directly.

What is the CSRD?

The Corporate Sustainability Reporting Directive (CSRD) is a new regulation from the European Union that aims to bring sustainability reporting up to the same level as financial reporting. In simple terms, it means that companies will now have to be more transparent and detailed about how their activities impact people and the planet, not just their profits.

As the EU’s Corporate Sustainability Reporting Directive (CSRD) transforms value chain transparency, Indian exporters must prepare for new demands from European partners.

What we’ve noticed is that many exporters are leaning heavily on industry associations and export promotion councils to understand what the CSRD means for them. But it’s largely happening on an ad hoc, "need-to-comply" basis. There’s no internalised system yet. No structured sustainability reporting mechanism that integrates with business strategy. And that’s exactly where the challenge lies.

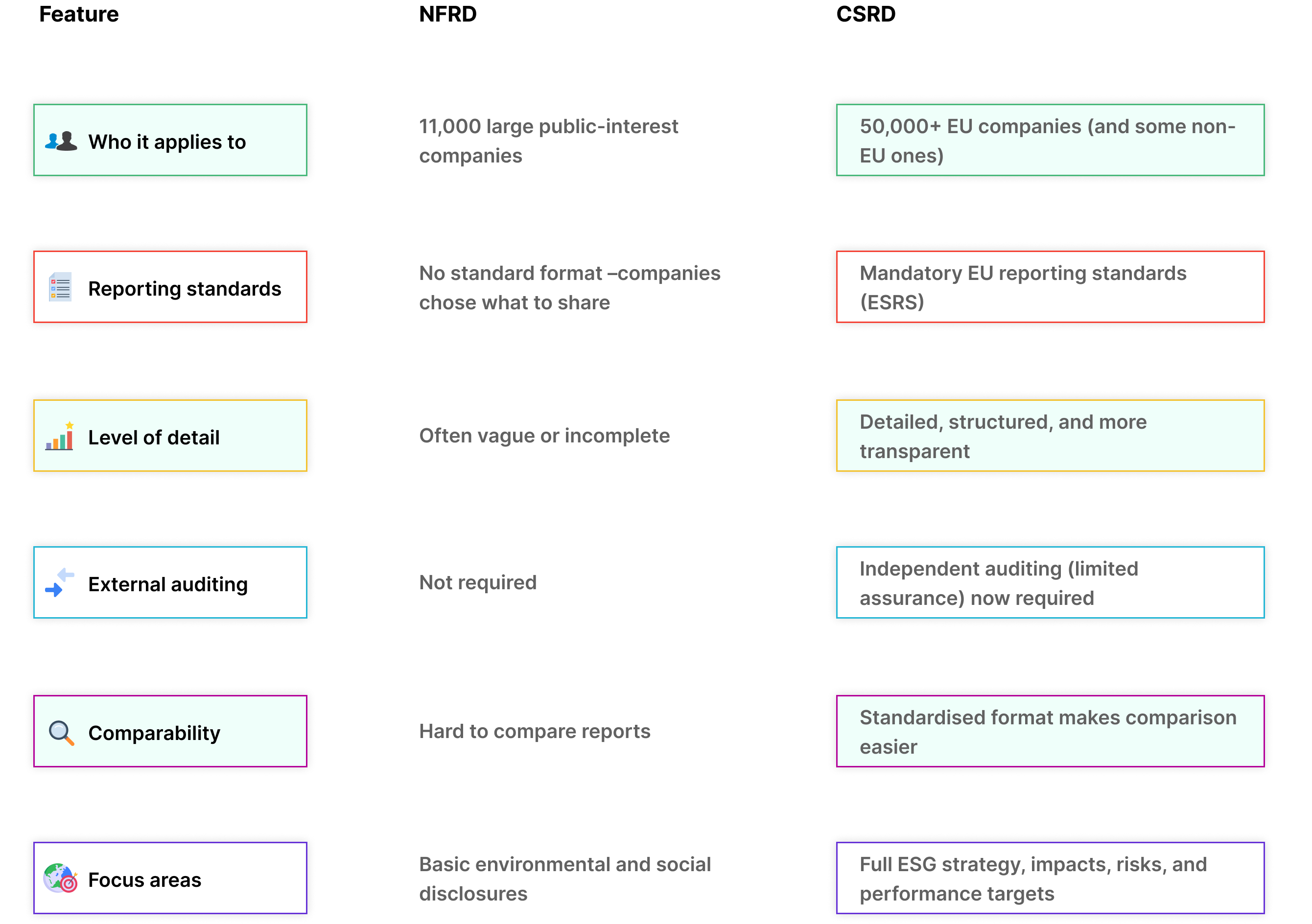

CSRD vs. Previous NFRD Rules

Before the CSRD, we had the Non-Financial Reporting Directive (NFRD) – and while it was a step in the right direction, it had some big gaps.

The CSRD takes sustainability reporting from “nice to have” to non-negotiable. It sets clear rules, applies to more companies, and demands real transparency.

Scope of CSRD compliance for non-EU suppliers

When talking to Indian exporters across sectors, one thing is clear, Europe remains a priority market. And the numbers back this up. The European Union is India’s second-largest trading partner, accounting for around €120 billion in goods trade in 2024. That’s roughly 11.5% of India’s total global trade.

Indian exports to the EU hit $93.08 billion last year, with the Netherlands, Germany, and Italy consistently among the top destinations. And this isn't just big business for the likes of Tata or Dr. Reddy’s, this trade is powered by thousands of firms across India, many of them mid-sized manufacturers, family-run operations, or fast-growing exporters who now find themselves integrated into European value chains.

Sectorally, the spread is wide and deep:

- Textiles and Apparel remain a powerhouse, contributing close to $9 billion annually. Many of these suppliers are in Tiruppur, Ludhiana, and Surat, where awareness of CSRD is still patchy at best.

- Machinery and Mechanical Appliances bring in between $6 –13 billion. These are often firms building precision components or assembly parts that plug directly into EU production lines.

- Chemicals and Pharma are right up there. $5.39 billion in organic chemicals and $3.54 billion in pharmaceutical products were exported in 2024. The EU remains one of the most tightly regulated destinations for both.

- Electronics and Electrical Equipment accounted for $12.68 billion, again with a mix of large corporates and Tier 2–3 suppliers in the chain.

- Then there’s Vehicles, Iron & Steel, and Mineral Fuels, each contributing billions more.

.png)

What this means on the ground is that a diverse ecosystem of Indian exporters, across industries and sizes, are now indirectly exposed to CSRD-driven demands. Whether they’ve heard the term or not, their buyers in Europe are under pressure to trace and report sustainability data, and that means the ask is coming downstream.

CSRD is not a trend; it’s the ticket. Get your reporting in order now, or watch your European market share slip to those who already have.

Why Should Indian Exporters Care?

Let’s clear something up right away: Your EU buyers will treat CSRD compliance as a gate pass. If you can’t show data, you risk exclusion.

Unless your company has a sizeable footprint in Europe, like a subsidiary or branch generating more than €150 million in annual EU turnover, you won’t be filing a CSRD report yourself. That’s the technical boundary.

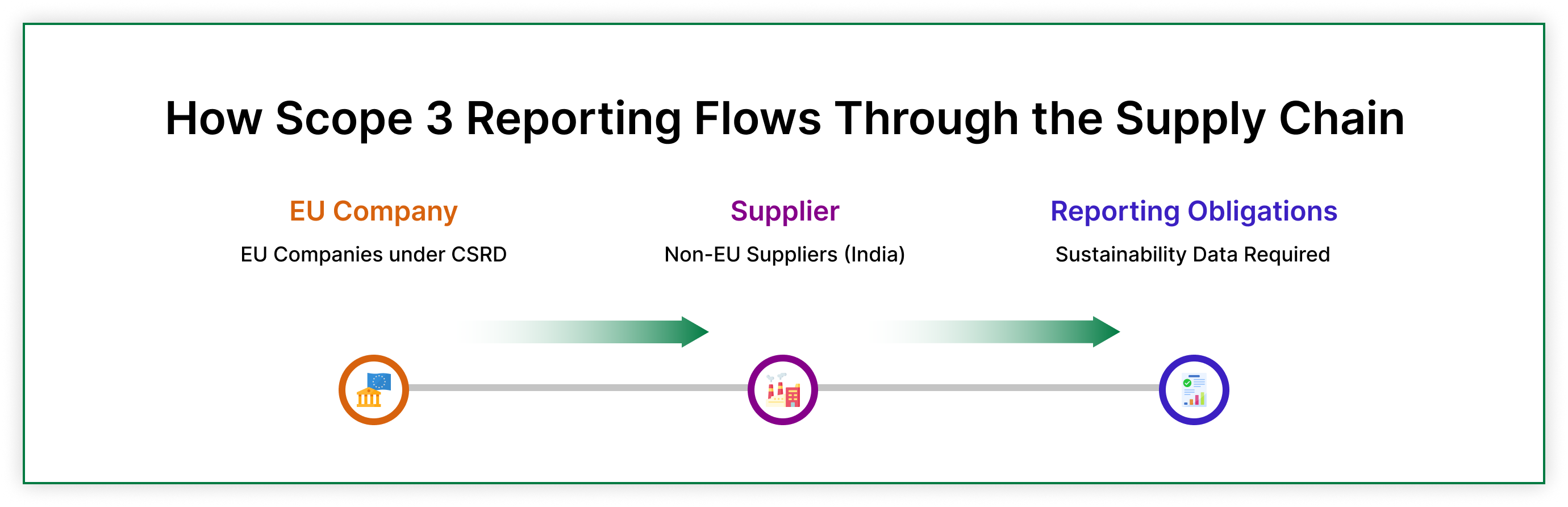

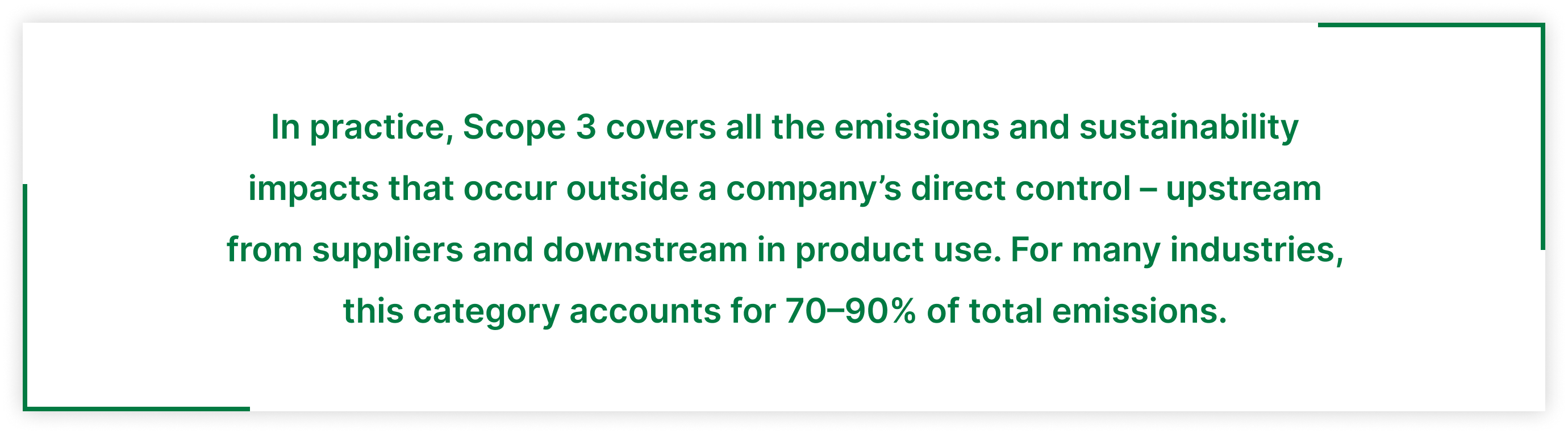

But here’s where it gets real. The CSRD isn’t just about who reports, it’s about what gets reported. And under its Scope 3 requirements, EU-based companies must disclose environmental and social impacts across their entire value chain. That includes you, the supplier, even if your office is in Ahmedabad or Vizag and you’ve never heard of ESRS.

Which is why EU importers are under pressure to go deeper into their supply chains, collect reliable ESG data, and prove they’re not blind to what’s happening outside their four walls.

Potential Consequences of Non-Compliance

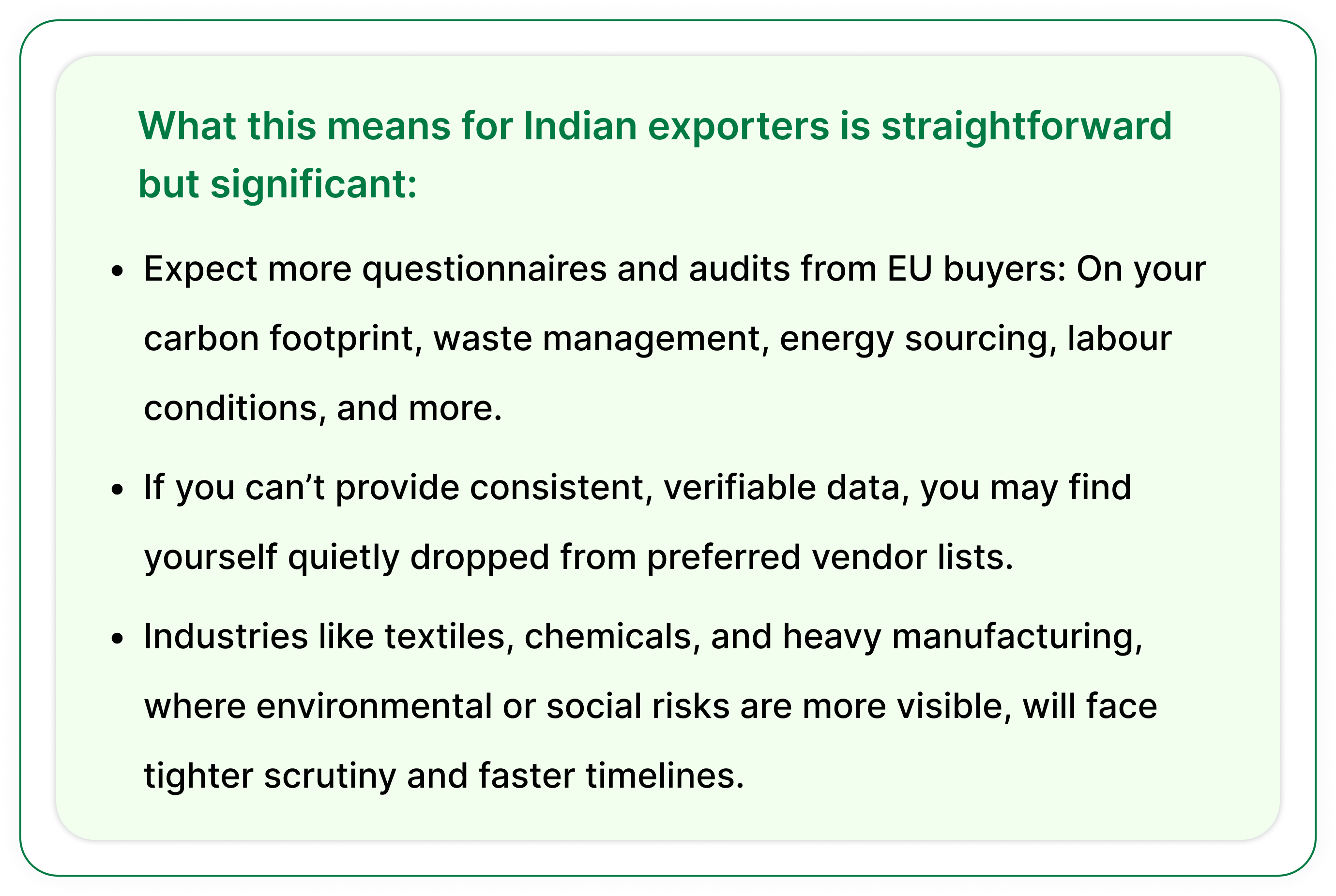

EU green regulations, including CSRD, are no longer just policy frameworks – they’re becoming hard entry requirements for market access. EU buyers are being pushed to trace emissions, social risks, and ethical practices across their value chains. That puts Indian suppliers under the lens.

If you can’t provide the data? You may not get the deal. If you can? You move up the shortlist.

We’re already seeing this shift play out. Indian firms that are proactive about sustainability reporting, especially those that can demonstrate verifiable Scope 3 data, are getting better terms, deeper buyer relationships, and in some cases, longer-term contracts. The EU CSRD impact on Indian exporters is becoming more visible – it’s not just a compliance issue anymore, but a strategic lever for growth and differentiation. Businesses that can align with these expectations early stand to benefit from increased credibility, while those who lag may lose out on key opportunities.

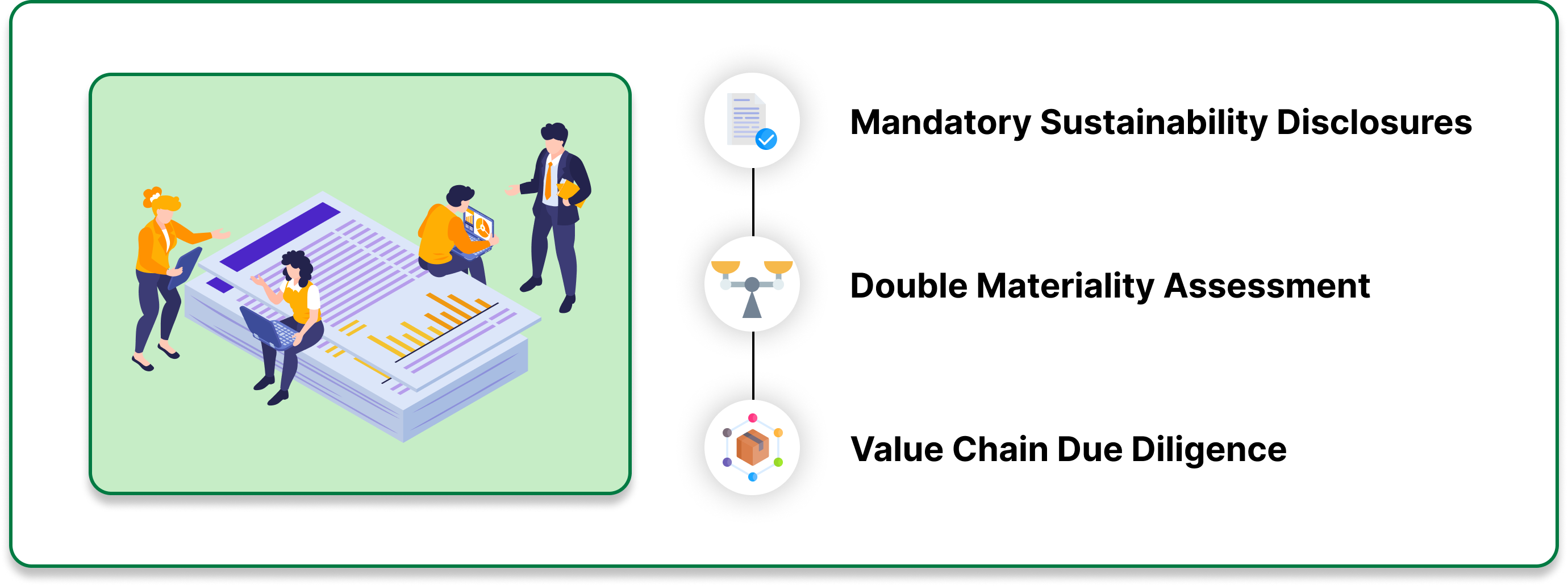

Key CSRD Requirements Affecting Non-EU Suppliers

The CSRD doesn’t just impact companies within the EU, it also extends its reach across global supply chains. Below are three key requirements that could significantly affect suppliers outside the EU.

1. Mandatory Sustainability Disclosures

Let’s start with the big one: reporting.

Under the CSRD, many companies in the EU are now legally required to report on a wide range of environmental, social, and governance (ESG) issues. This includes everything from carbon emissions to labour practices and water use.

Here’s where it matters to non-EU suppliers: EU companies need to report on their entire value chain. That includes you. Even if you’re not based in the EU, your clients may start asking for detailed sustainability data. Not just high-level statements – real numbers, documentation, and proof. If you haven’t been tracking your emissions or supply chain risks before, now’s a good time to start. It won’t just help your EU partners; it’ll help you stay competitive.

Manual spreadsheets won’t scale. Platforms like KarbonWise simplify supplier input collection, create audit-ready data trails, and align with ESRS.

2. Double Materiality Assessment

"Double materiality" might sound technical, but the idea is simple.

EU companies now have to look at sustainability from two perspectives:

- How environmental and social issues affect their business?

- How their business affects people and the planet?

That means EU companies can’t just look inward, they also need to assess the impact of their suppliers and partners. So, if your operations have a high carbon footprint or weak labour protections, those risks will show up in their reports. Your sustainability practices are no longer just your business. They’re part of your clients’ reporting obligations, too.

KarbonWise maps both business impacts (financial risks) and footprint impacts (Scope 3, waste and labour practices) onto one reporting-ready system.

3. Value Chain Due Diligence

This is where things get more hands-on.

The CSRD requires companies to actively identify, address, and manage sustainability risks across their value chains. You might see more requests for audits, codes of conduct, or proof of ethical sourcing. Companies may ask about your raw materials, worker safety policies, or climate targets.

Being ready, transparent, and open to collaboration will go a long way. That’s where supplier engagement modules, automated reminders, and traceability functions come in, helping avoid endless back-and-forth emails.

Steps Indian Businesses Should Take

If you’re exporting to Europe, here’s what needs to be on your radar immediately:

{{flipcards}}

The EU has drawn a new line in the sand. The businesses that cross it early will not only protect their position in European markets but will also stand out as credible, future-ready partners across the global stage. The ones who wait may find that the doors start closing quietly, without warning.

Conclusion: Proactively Preparing for the New EU Sustainability Landscape

This isn’t just a Europe story. India is tightening its own ESG regime too. The SEBI-mandated Business Responsibility and Sustainability Reporting (BRSR) is now mandatory for the top 1,000 listed companies, and the others will be roped in sooner or later.

Companies that begin aligning their internal systems with CSRD-compatible standards now will be better positioned for cross-market compliance – reducing duplication, audit fatigue, and last-minute scrambling. It’s a case of building once, benefiting twice.

Banks and investors too aren’t waiting for regulations to catch up. Across the board, reports suggest lower cost of capital, faster access to green finance, and even valuation premiums for firms that can prove ESG alignment – especially in high-impact sectors. Scope 3 transparency is becoming a checkbox for sustainable finance, and those who treat it as a reporting afterthought will struggle to qualify.

Bottom line: whether it’s about maintaining market access, staying attractive to investors, or de-risking operations, CSRD isn’t just a regulatory challenge – it’s a competitive opportunity, especially for exporters willing to think two steps ahead.

{{accordion}}

{{sources}}

Continue Reading

SBTi FLAG Guidance v1.2: What Changed and What to Do Next

Learn what's new in SBTi FLAG Guidance v1.2, including updated deadlines, mandatory commodities, no-deforestation requirements, and practical steps for businesses.

How to conduct a double materiality assessment: A practical step-by-step guide (2026)

Learn how to conduct a Double Materiality Assessment with this practical step-by-step guide covering impact and financial materiality, IROs, stakeholder engagement, scoring, materiality matrices, and ESG reporting.

.avif)

.svg)

.svg)