Introduction to Carbon Border Taxes

Carbon border taxes are transforming global trade by assigning a carbon cost to imported goods based on embedded emissions. Learn how CBAM works, its impact on supply chains, and how businesses can prepare for evolving compliance requirements.

.svg)

Table of Contents

Climate policy is increasingly influencing how countries trade with one another. As governments strengthen climate targets and introduce carbon pricing systems, they are also beginning to address the emissions embedded in imported goods. This is where carbon border taxes come into play.

Carbon border taxes, often called border carbon adjustments, apply a carbon cost to imported products based on the emissions generated during their production. The aim is to ensure that imported goods face a similar carbon price to products manufactured domestically under climate regulations. Without such measures, industries operating in regions with strict emissions policies could face unfair competition from producers in countries with weaker environmental rules.

The idea is closely tied to carbon pricing. Many economies already charge companies for the greenhouse gases they emit through carbon taxes or emissions trading systems. However, these policies can create the risk of carbon leakage, where production shifts to jurisdictions with lower climate standards.

As a result, governments are beginning to integrate climate policy with trade regulation. The European Union has already introduced a Carbon Border Adjustment Mechanism, and several other economies are exploring similar policies. For businesses involved in global supply chains, carbon border taxes are quickly becoming an important part of the trade landscape.

Understanding the Carbon Border Adjustment Mechanism (CBAM)

The Carbon Border Adjustment Mechanism, commonly known as CBAM, is the European Union’s policy designed to place a carbon cost on certain imported goods. It works alongside the EU’s existing carbon pricing system to ensure that products entering the EU market reflect the emissions generated during their production.

In simple terms, CBAM requires importers to report the greenhouse gas emissions embedded in specific products and, over time, pay a carbon price that mirrors what EU manufacturers face under the EU Emissions Trading System. The objective is to prevent carbon leakage, where companies move production to regions with weaker climate regulations while continuing to sell goods in markets with stricter policies.

CBAM initially applies to sectors that are both carbon-intensive and heavily traded internationally. These include cement, iron and steel, aluminium, fertilisers, electricity and hydrogen. These industries were selected because their production processes generate significant emissions and they face higher risks of carbon leakage.

The mechanism is being introduced in phases. During the transitional reporting period, importers are required to submit quarterly reports detailing the embedded emissions in covered products. At this stage, no carbon payment is required. From the full implementation phase onward, importers will need to purchase CBAM certificates corresponding to the emissions associated with their goods.

CBAM is closely linked to domestic carbon pricing within the EU. As European producers pay for emissions through the EU Emissions Trading System, CBAM ensures that imported products face a comparable carbon cost. This alignment aims to maintain fair competition while encouraging global producers to reduce the carbon intensity of their manufacturing processes.

Why Carbon Border Taxes Matter for Global Trade

Carbon border taxes are beginning to reshape how goods move across international markets. As carbon pricing policies expand, trade regulations are increasingly being used to ensure that climate policies do not distort competition or shift emissions across borders. For companies involved in global manufacturing and exports, these policies are becoming an important strategic factor.

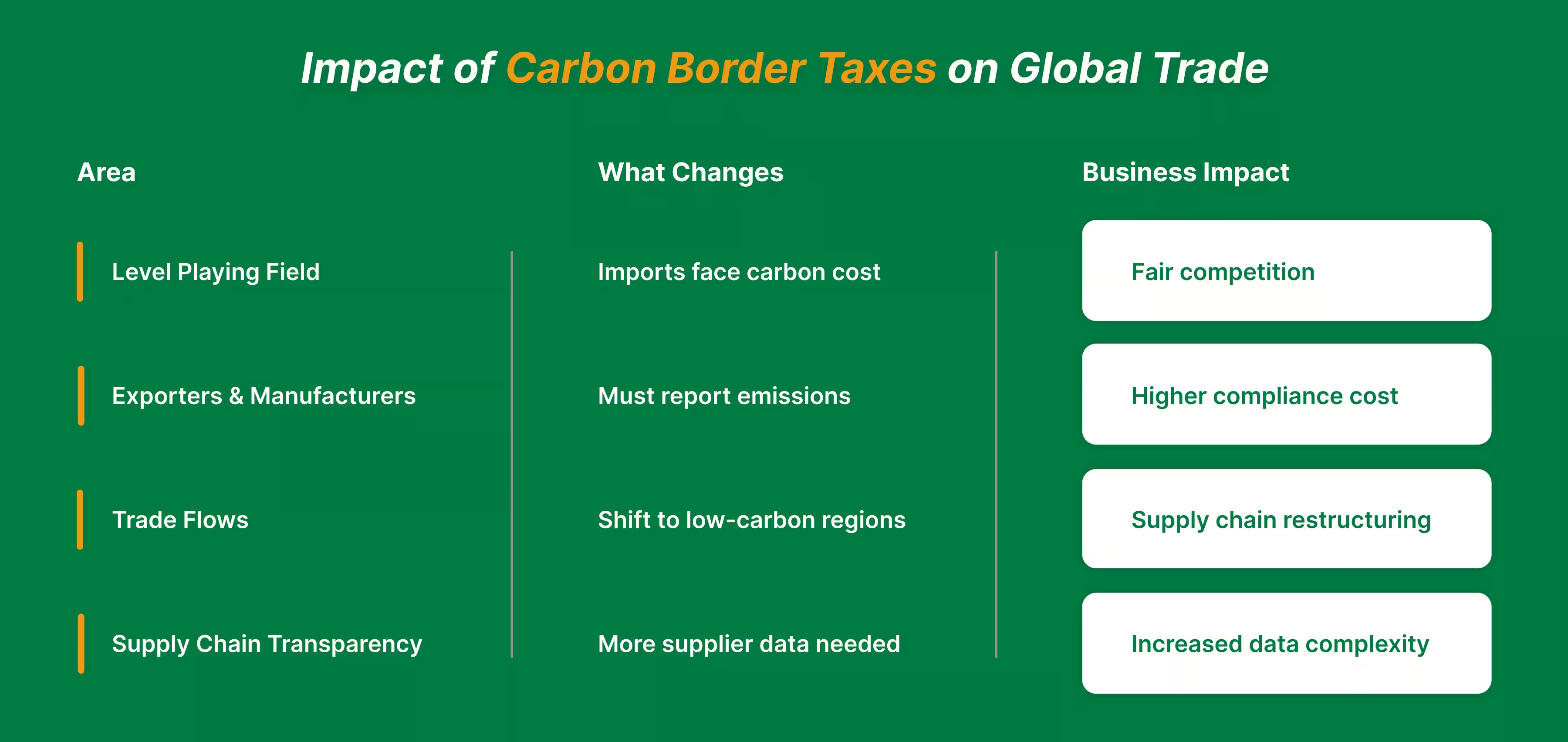

Leveling the Playing Field

One of the primary objectives of carbon border taxes is to prevent carbon leakage. When countries introduce strict climate policies or carbon pricing systems, domestic producers may face higher production costs. Without border adjustments, companies could shift manufacturing to regions with weaker climate regulations while continuing to export products back into regulated markets.

Carbon border taxes aim to address this imbalance. By applying a comparable carbon cost to imported goods, they ensure that domestic and foreign producers compete under similar environmental conditions. This helps maintain fair competition while reinforcing climate policies.

Impact on Exporters and Manufacturers

For exporters and manufacturers, carbon border taxes introduce new compliance obligations. Companies exporting to markets with border adjustment mechanisms must now calculate and report the emissions embedded in their products. This often requires detailed data on energy consumption, production processes and raw materials.

In addition to reporting requirements, businesses may face higher costs if their products have a high carbon intensity. Exposure to carbon pricing through border mechanisms means that emissions performance can directly influence trade competitiveness.

Trade Flow Shifts

Carbon pricing in trade policy is also influencing sourcing and production decisions. Companies may begin to reassess where goods are manufactured and where raw materials are sourced. Regions with lower carbon intensity production may become more attractive as companies attempt to minimise exposure to carbon border costs.

These pressures are already contributing to broader discussions around regionalisation and nearshoring. Firms may increasingly favour suppliers located in regions with comparable climate regulations and lower emissions profiles.

Supply Chain Transparency Requirements

Carbon border taxes also increase the demand for supply chain transparency. Importers must be able to demonstrate the emissions associated with their products, which often requires collecting data from multiple suppliers.

This creates a growing need for accurate Scope 1, Scope 2 and Scope 3 emissions data. Companies are also facing greater expectations to obtain reliable disclosures from suppliers, particularly in carbon-intensive industries. As a result, emissions reporting and supply chain visibility are becoming critical components of international trade compliance.

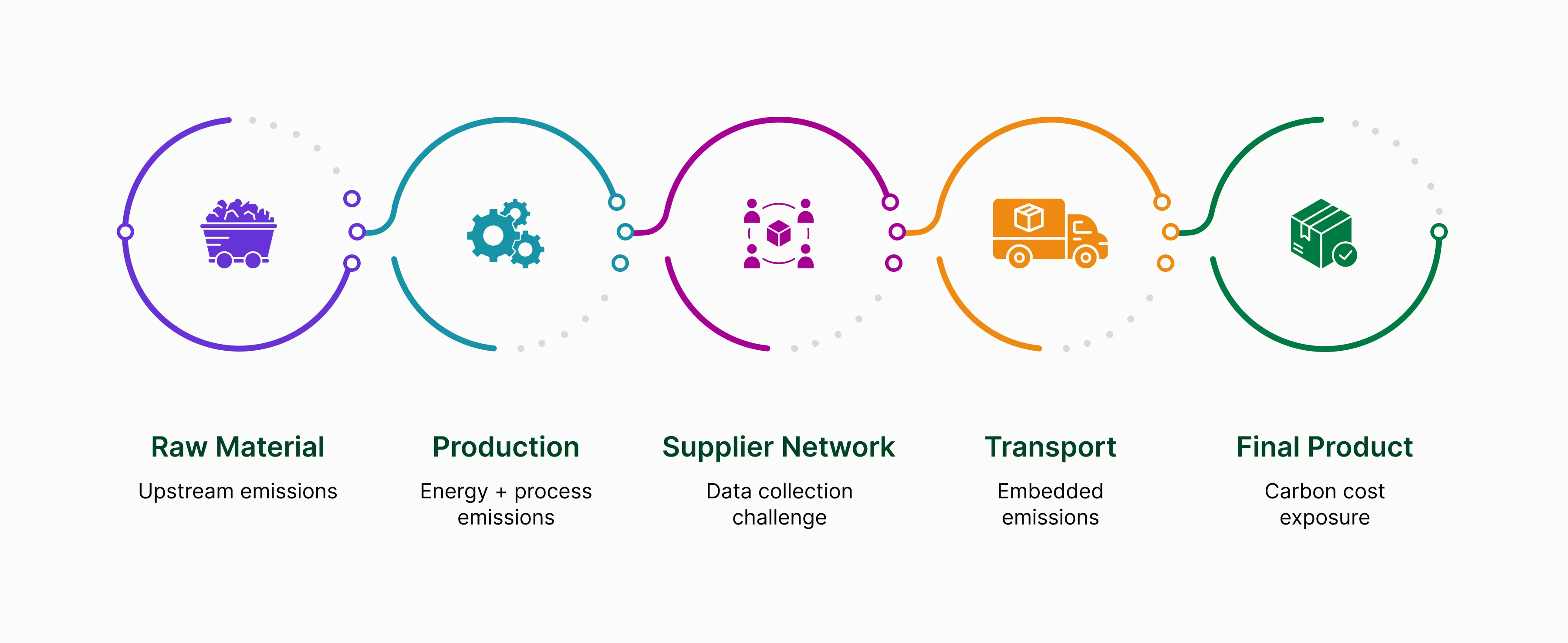

How Carbon Border Taxes Are Reshaping Supply Chains

Carbon border taxes are pushing companies to rethink how supply chains are measured, managed and optimised. Because these mechanisms calculate costs based on the emissions embedded in products, businesses can no longer focus only on operational emissions within their own facilities. The carbon intensity of upstream suppliers and production processes is now directly linked to trade competitiveness.

Embedded Emissions Measurement

A central requirement under mechanisms such as CBAM is the calculation of embedded emissions at the product level. Importers must quantify the greenhouse gases generated during production, particularly from energy use and industrial processes. For sectors such as steel, aluminium and cement, this involves measuring direct process emissions as well as electricity-related emissions associated with manufacturing.

Life Cycle Assessment is increasingly used to support this process. LCA frameworks allow companies to evaluate emissions across production stages and identify the processes contributing most to embedded carbon. This level of measurement is becoming essential for exporters who need to report emissions accurately when accessing regulated markets.

Supplier Engagement and Data Collection

Carbon border taxes also increase the importance of supplier data. Importers cannot rely solely on generic emission factors if regulators require verified product-level emissions. As a result, companies must work more closely with suppliers to obtain primary data on energy consumption, fuel use and production processes.

Managing this information becomes more complex in multi-tier supply chains. Manufacturers often depend on suppliers across several countries, each operating under different reporting standards. Establishing consistent data collection systems and supplier disclosure requirements is becoming a priority for companies exporting to regulated markets.

Procurement Strategy Transformation

Procurement decisions are also evolving as carbon costs begin to influence sourcing strategies. Buyers are increasingly evaluating suppliers not only on price and quality but also on emissions intensity. Suppliers using renewable energy or lower-carbon production technologies may become more attractive because they reduce the carbon exposure associated with imported goods.

Companies are also beginning to incorporate carbon pricing assumptions into procurement models. This allows organisations to anticipate how carbon border mechanisms could affect the total cost of goods over time.

Decarbonisation as a Competitive Advantage

Reducing embedded emissions is becoming a strategic advantage in carbon-regulated markets. Companies that lower the carbon intensity of their products can reduce potential border tax liabilities and maintain price competitiveness.

This shift is also reinforcing broader corporate net-zero commitments. Investments in cleaner technologies, renewable energy sourcing and process efficiency improvements not only support climate targets but also help companies adapt to emerging carbon-based trade regulations.

Compliance Requirements and Reporting Considerations

Carbon border taxes introduce new compliance obligations for companies exporting goods into regulated markets. Mechanisms such as the EU’s Carbon Border Adjustment Mechanism require importers to demonstrate how emissions associated with their products are calculated and reported. This means businesses must adopt clear methodologies, maintain proper documentation and ensure that emissions data can withstand regulatory scrutiny.

One of the first requirements is applying recognised emissions calculation methodologies. Companies must quantify the greenhouse gases generated during production, including direct emissions from industrial processes and indirect emissions from electricity consumption. In many cases, regulators expect calculations to follow established frameworks such as the Greenhouse Gas Protocol or methodologies aligned with international climate reporting standards. Where primary supplier data is unavailable, default emission factors may be used, but these often lead to higher reported emissions and therefore greater carbon cost exposure.

Documentation is equally important. Importers must maintain detailed records showing how emissions were calculated, which data sources were used and how system boundaries were defined. Regulators may require supporting evidence such as production data, energy consumption records and supplier disclosures. In some cases, third-party verification may also be required to confirm the accuracy of emissions reporting.

Alignment with international standards helps strengthen compliance. Companies that structure their emissions accounting according to recognised frameworks are better positioned to adapt to evolving regulatory requirements across different markets.

Failure to meet reporting obligations can lead to financial penalties, delayed imports or reputational risks. As carbon-based trade policies expand, accurate emissions reporting and transparent documentation are becoming critical components of global trade compliance.

Best Practices for Managing Carbon Border Tax Risk

As carbon border taxes expand, companies involved in international trade need structured strategies to manage potential exposure. Preparing early can reduce compliance risk, prevent unexpected costs and strengthen supply chain resilience. Several practical steps can help organisations adapt to carbon-based trade regulations.

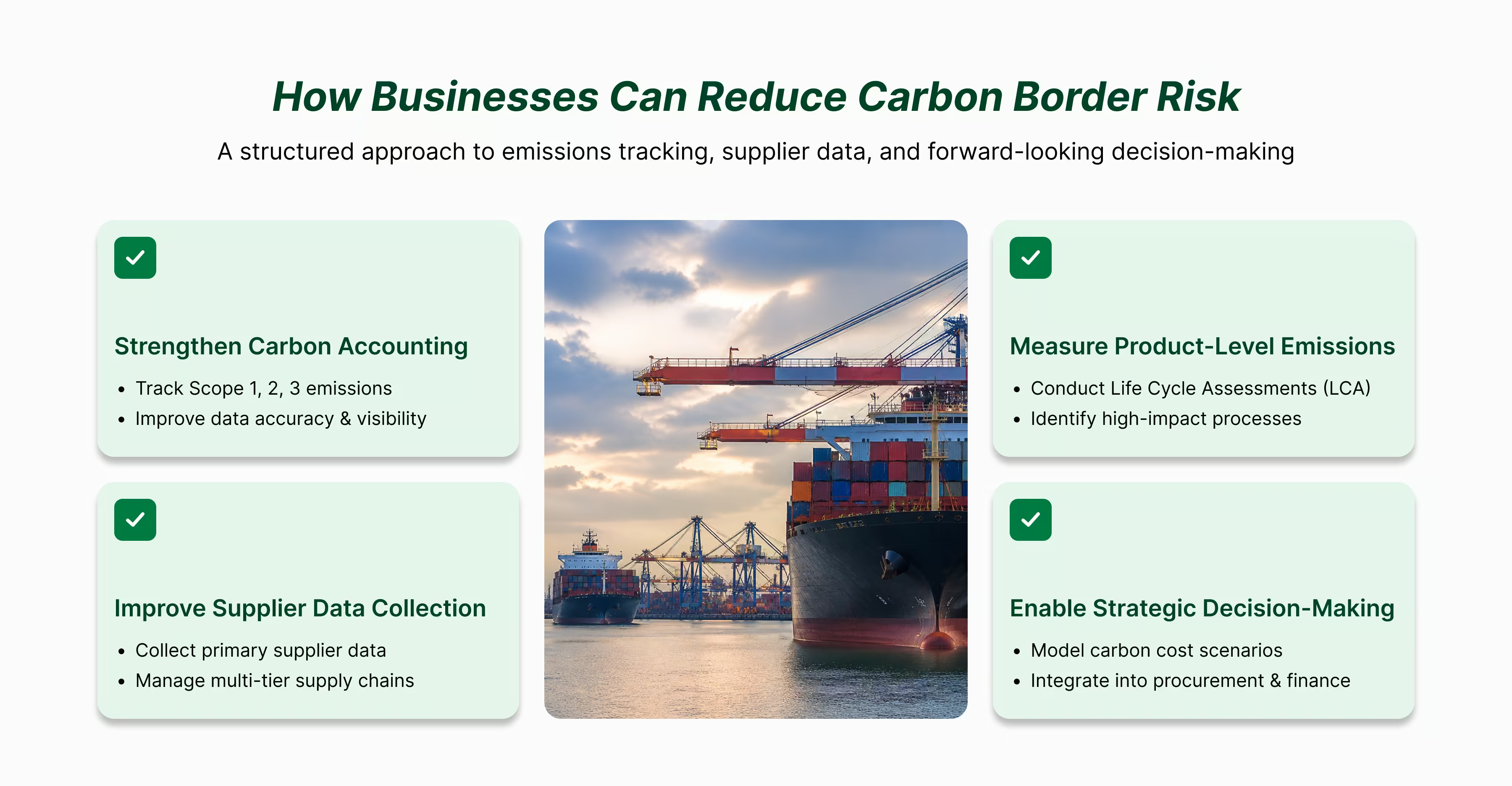

Strengthening Carbon Accounting Systems

A reliable carbon accounting system is the foundation for managing border tax exposure. Companies need accurate tracking of Scope 1, Scope 2 and, increasingly, Scope 3 emissions across their operations and supply chains. This requires consistent data collection from production facilities, energy use records and supplier disclosures.

Many organisations are also moving towards more frequent monitoring of emissions data rather than relying solely on annual reporting. Better visibility into operational emissions allows companies to identify carbon-intensive processes and respond more quickly to regulatory requirements.

Conducting Product-Level LCAs

Product-level Life Cycle Assessments are becoming increasingly valuable under carbon border mechanisms. These assessments allow companies to calculate the emissions associated with specific products, including raw material extraction, manufacturing and energy consumption.

By identifying high-impact processes within the production cycle, businesses can prioritise improvements such as energy efficiency upgrades, material substitutions or cleaner production technologies. Lowering product-level emissions can directly reduce exposure to carbon border costs.

Building Cross-Functional Governance

Carbon border taxes affect multiple functions within an organisation. Sustainability teams may lead emissions measurement, but finance teams must evaluate potential carbon costs while trade and compliance teams manage reporting requirements.

Effective governance requires coordination between these departments. Integrating carbon pricing considerations into financial planning and procurement strategies helps ensure that climate policy risks are reflected in business decisions.

Scenario Planning and Risk Assessment

Forward-looking analysis is also important. Companies can model how different carbon price levels or regulatory changes might affect the cost of exporting certain products. This helps organisations understand where risks are concentrated within their portfolio.

Scenario analysis can also support strategic sourcing decisions. Businesses may explore alternative suppliers, lower-carbon production methods or regional manufacturing options to reduce exposure to future carbon border taxes.

Case Examples: Businesses Adapting to Carbon Border Taxes

As carbon border policies begin to take effect, several companies in carbon-intensive industries are already adjusting their operations, compliance systems and supply chain strategies. These changes are particularly visible in sectors such as steel, cement and automotive manufacturing, where emissions intensity directly influences trade competitiveness.

These examples illustrate how carbon border taxes are already influencing corporate strategy. Companies that reduce embedded emissions, strengthen emissions reporting systems and work closely with suppliers are better positioned to adapt to emerging carbon-based trade regulations.

Tools and Resources for Carbon Border Tax Compliance

Carbon border regulations require companies to calculate product-level emissions, maintain verifiable documentation and report data according to defined regulatory formats. To meet these requirements, businesses rely on several types of tools and guidance frameworks.

Carbon accounting software platforms are commonly used to collect and organise emissions data across operations and supply chains. These systems support the calculation of Scope 1 and Scope 2 emissions from production facilities and can also integrate supplier data relevant to Scope 3 emissions. For exporters affected by border carbon mechanisms, structured carbon accounting systems help consolidate the operational and supplier information needed for emissions reporting.

Life Cycle Assessment and product carbon footprint tools are also important because border adjustment mechanisms often require emissions to be calculated at the product level. LCA methodologies allow companies to quantify emissions associated with raw material extraction, manufacturing processes and energy consumption. These calculations are particularly relevant for sectors covered under carbon border mechanisms, including steel, aluminium, cement and fertilisers.

Regulatory guidance documents issued by governments and policy bodies provide the technical rules for emissions calculation and reporting. For example, the European Commission has published detailed guidance for the Carbon Border Adjustment Mechanism covering reporting formats, emissions calculation methods and sector-specific requirements. These documents outline how importers must calculate embedded emissions and submit compliance reports.

Trade compliance advisory services are often used by companies exporting into regulated markets. These services help organisations interpret regulatory obligations, establishemissions reporting systems and prepare documentation for verification or regulatory review. Together, these tools support the technical and administrative requirements associated with carbon border tax compliance.

Conclusion

Carbon border taxes are beginning to reshape how international trade operates. By linking the cost of imports to the emissions generated during production, these policies are pushing businesses to account for the carbon intensity of their products and supply chains. Mechanisms such as the Carbon Border Adjustment Mechanism illustrate how climate policy is increasingly being integrated into global trade regulation.

For exporters and manufacturers, this shift means emissions management is no longer only an environmental concern. It is becoming a commercial and compliance issue. Companies that can measure embedded emissions accurately, report them according to regulatory requirements and reduce carbon intensity across their operations will be better positioned to compete in markets adopting carbon border mechanisms.

This transition also places greater emphasis on supply chain transparency. Businesses must increasingly work with suppliers to obtain reliable emissions data and strengthen visibility across multi-tier supply networks. Accurate data collection, structured carbon accounting and product-level emissions analysis are becoming essential capabilities for companies engaged in international trade.

Platforms such as KarbonWise can support this process by helping organisations measure emissions, manage carbon data and track supply chain impacts more effectively. By integrating carbon accounting, emissions monitoring and reporting capabilities in a single system, KarbonWise enables businesses to prepare for evolving regulatory requirements while improving overall emissions visibility.

If your organisation is preparing for carbon border regulations or looking to strengthen emissions reporting across global operations, request a demo to see how KarbonWise can help streamline carbon data management and support trade compliance.

{{cta}}

{{accordion}}

{{sources}}

Continue Reading

CBAM in 2026: The Cost Is Small Today. Here Is Exactly How It Compounds

CBAM costs may seem small today, but they increase significantly over time. Discover how the phase-in schedule, default values, and compliance obligations affect exporters through 2034.

CBAM 2026: Why Emissions Data Will Decide EU Market Access

From 2026, CBAM becomes a financial obligation. Verified emissions data will directly determine carbon costs, pricing competitiveness, and continued EU market access for exporters.

CBAM Compliance for Indian Exporters: What you need to know about CBAM and EU Carbon Tariffs

A practical guide for Indian exporters on understanding and complying with the EU’s Carbon Border Adjustment Mechanism (CBAM). Learn how carbon tariffs impact key sectors like steel and aluminium, what emissions data must be reported, and how exporters can prepare through accurate measurement, verification, and decarbonisation strategies.

.avif)

.svg)

.svg)